🇯🇵 How does Japan protect bank deposits when banks fail?

🇯🇵 How does Japan protect bank deposits when banks fail? 🤯 Their deposit insurance system handled 180+ financial institution failures, including the massive 90's banking crisis 👉 Here's how Japan's ¥10M deposit guarantee scheme works: https://illya.sh/blog/posts/deposit-guarantee-scheme-japan-dia-dicj/ 🧵

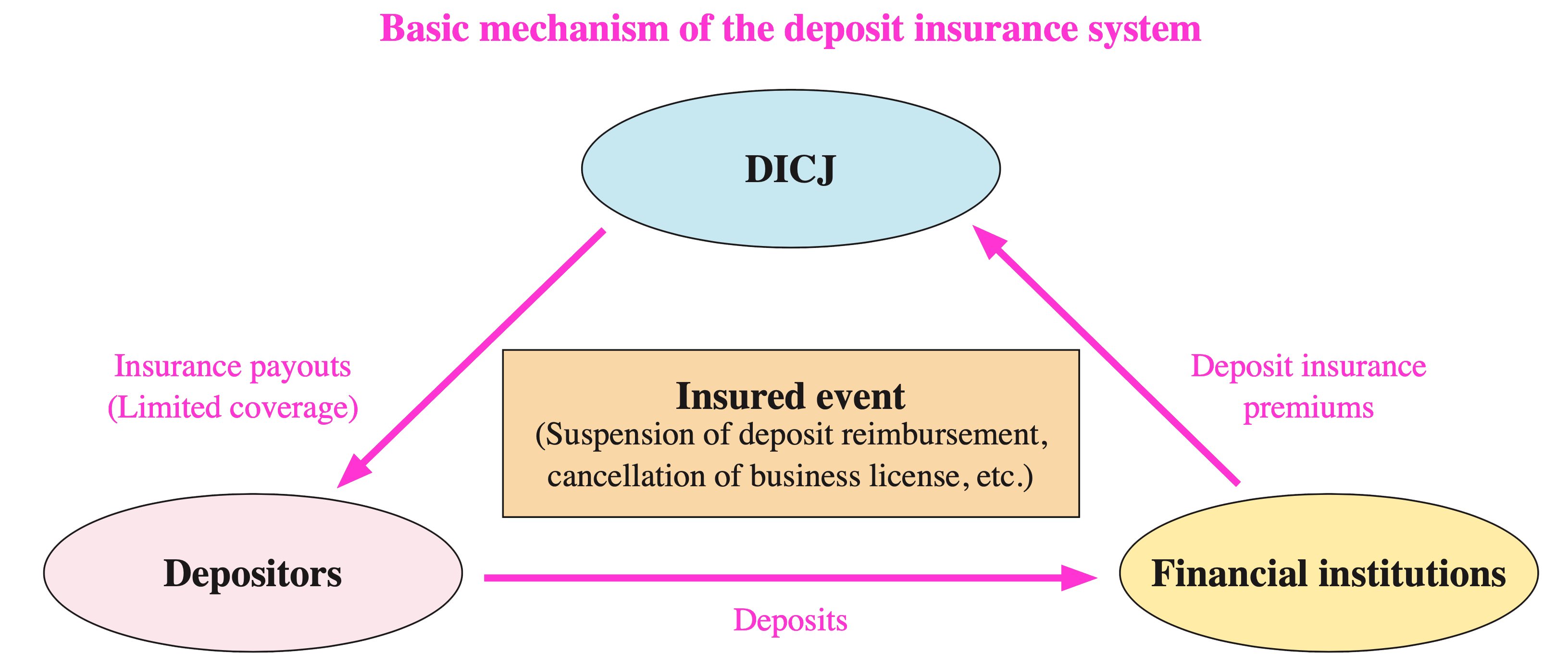

🏦 The Deposit Insurance Corporation of Japan (DICJ), provisioned in the Deposit Insurance Act (DIA) defines as its goals: • Deposit insurance • Financial system stability • Troubled financial institution resolution Deposits guarantee is just one of responsibilities

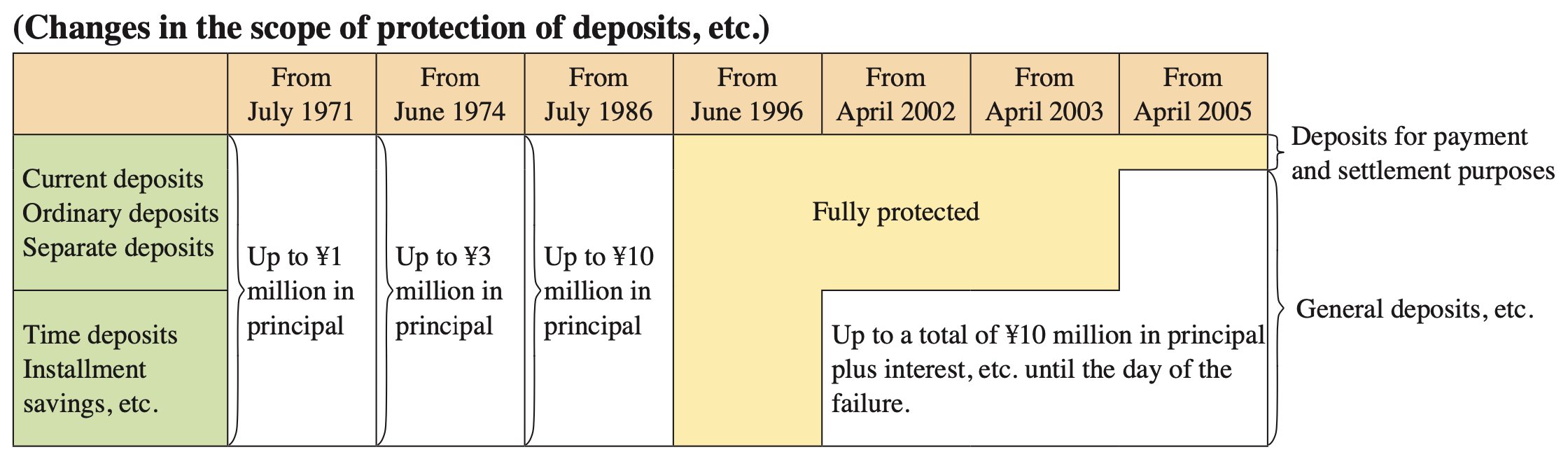

💴 Coverage limits: • Regular deposits: Up to ¥10M (~$65k/€60k) • Payment & settlement accounts: 100% covered 💡Fun fact: During the 90s crisis, ALL deposits were fully protected. Japan gradually reduced this to ¥10M by 2005

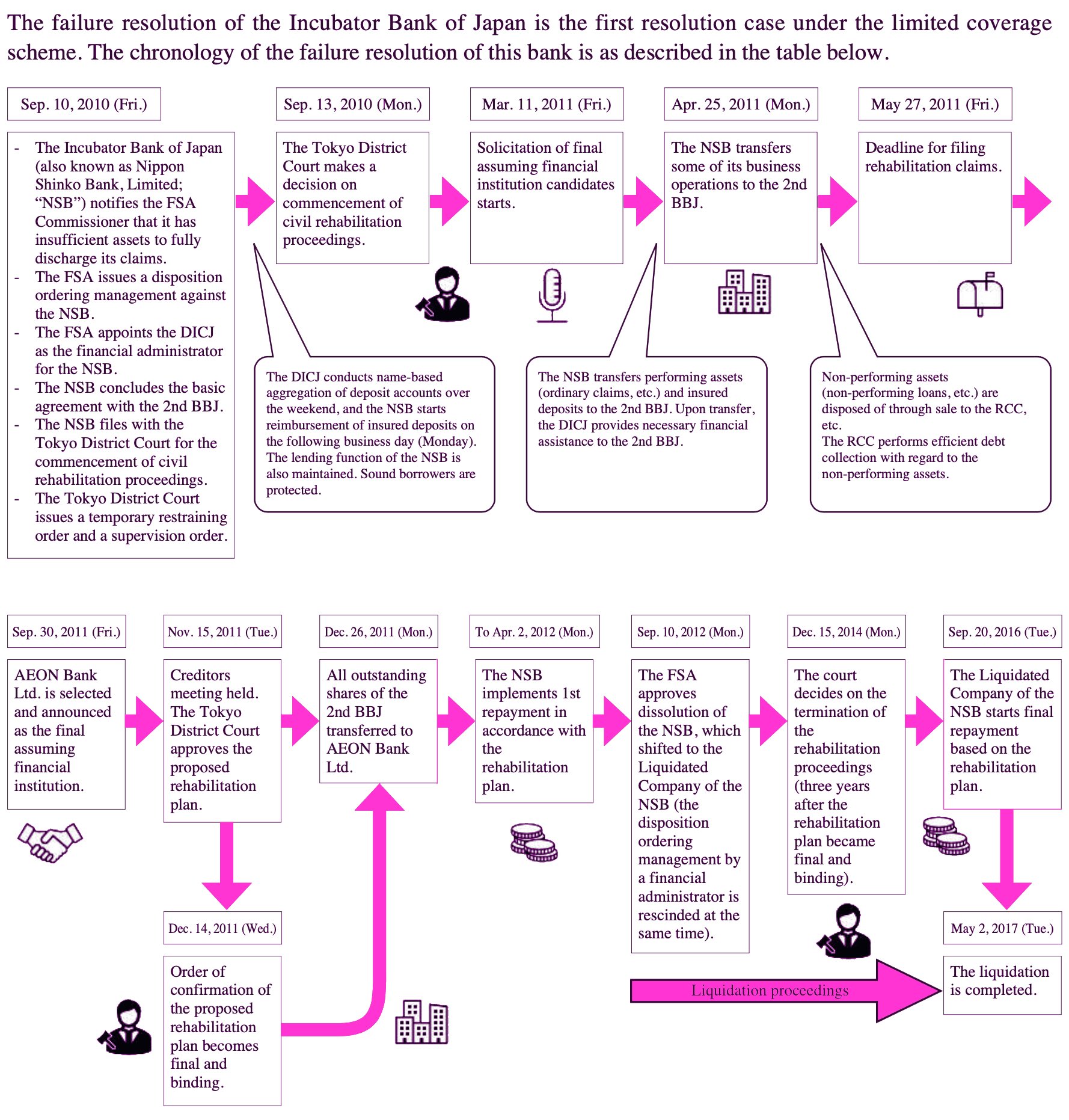

🚀 How fast do you get your deposits back? The Incubator Bank case (2010) shows DICJ timeline in practice: • Bank failed on Friday • Deposits returned by Monday 3 days/by next working day to have insured deposits available 🤝

💰 DICJ's funding comes from: • Self-issued bonds • Insurance premiums paid by banks • Borrowed funds from financial institutions & public In practice, operation financing is heavily relied on debt, making it risky long-term 📈

🇯🇵🆚🇪🇺 Japan's & EU's deposit guarantee schemes differ⬇️ 🇯🇵 DICJ: Active crisis manager (Act 34 of 1971) 🇪🇺 DGS: Mainly deposit protection (Directive 2014/49/EU) Japan's approach = more intervention power & broader mandate EU's approach = more focused mandate

🚨 The system faced its biggest test during the 90s banking crisis: • 110 financial institutions resolved • Full deposit protection implemented • Massive debt-based interventions DICJ has met its insurance obligations, but at what cost? 🤔

🇯🇵⚠️ Current risks: • Heavy reliance on debt • Large US Dollar & Securities exposure • Currency devaluation, leading to inflation These could trigger a 90s-style crisis 2.0 📉

🎌 While Japan has been successful in resolving hundreds of financial institution failures, the debt-heavy approach can only be only effective if the value created by credit is larger than the principal Otherwise, there's another bubble building up 🫧

🇯🇵🧠 For a deeper dive into Japan's deposit insurance system, read or listen my article at https://illya.sh/blog/posts/deposit-guarantee-scheme-japan-dia-dicj/ It covers Japan's deposit insurance's: • Legal framework • Historical cases • Risk analysis • EU comparison Got questions? Ask me! 👇