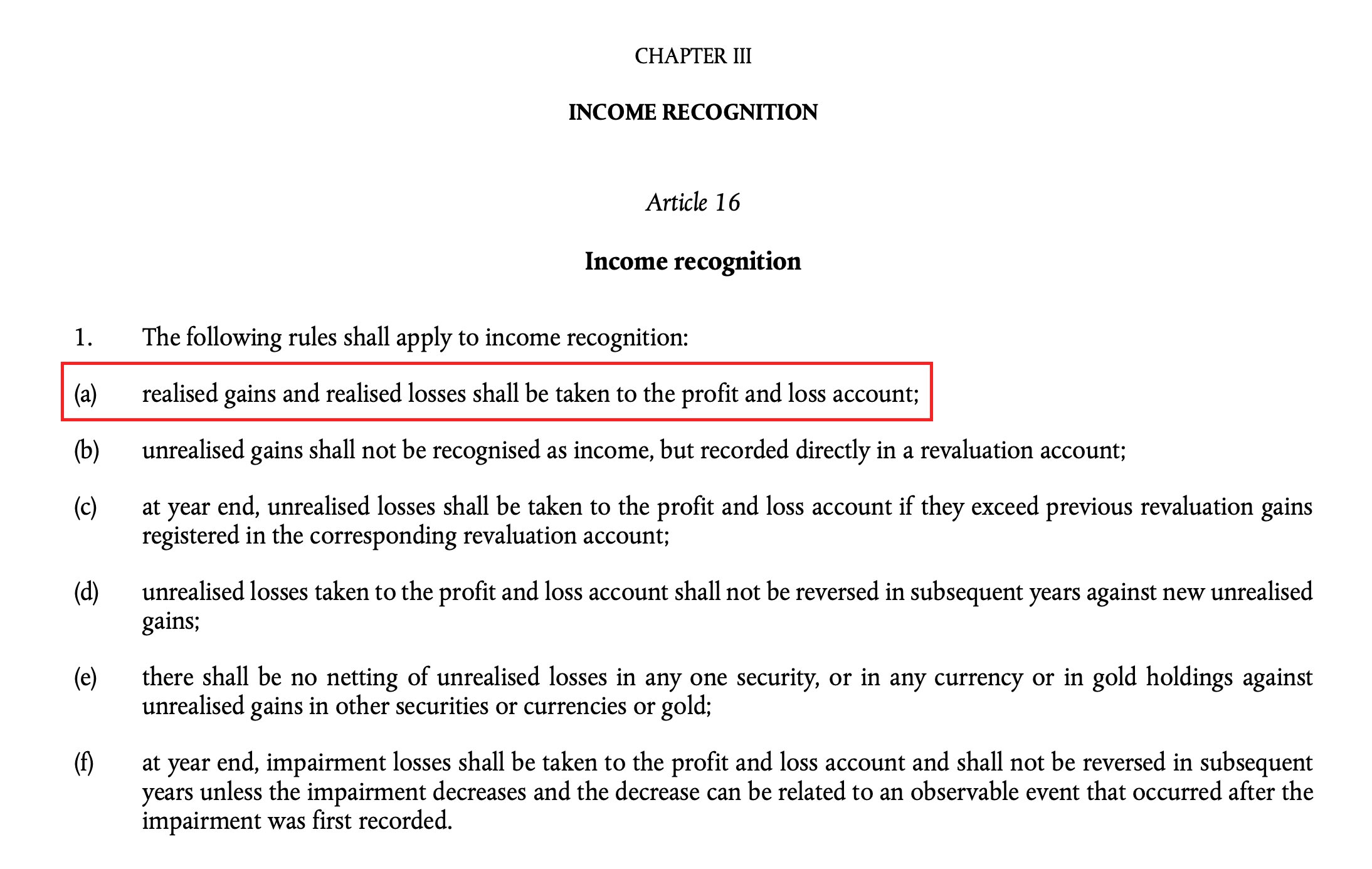

ECB's legal framework forbids the use of gold revaluation proceeds to pay expenses or operating losses

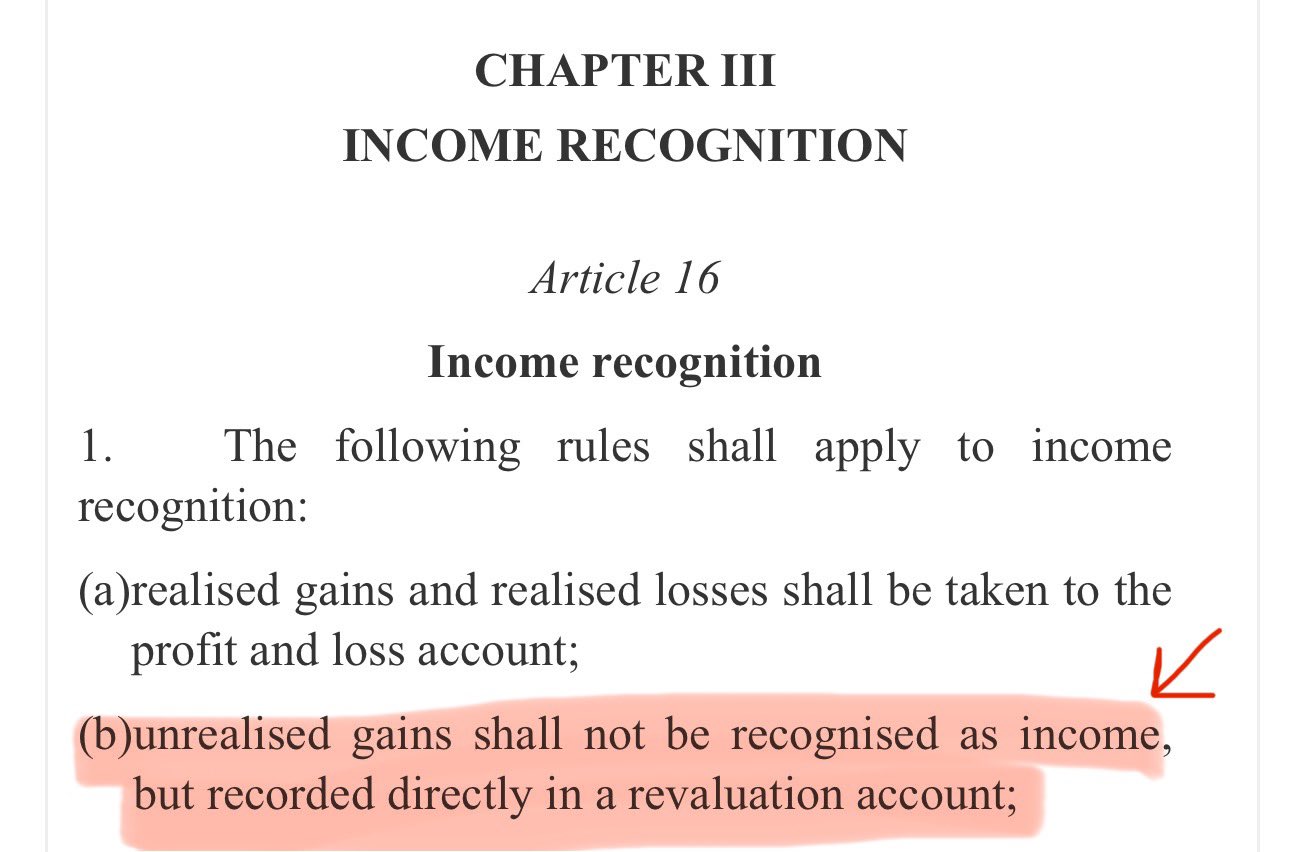

ECB's legal framework forbids the use of gold revaluation proceeds to pay expenses or operating losses unrealized gains are not recognized as income and are instead credited to the revaluation account revaluation account is under liability/equity on the ECB's balance sheet

moreover, as per Eurosystem's accounting framework unrealized gains are non-distributable and may only offset future unrealized losses on the same item

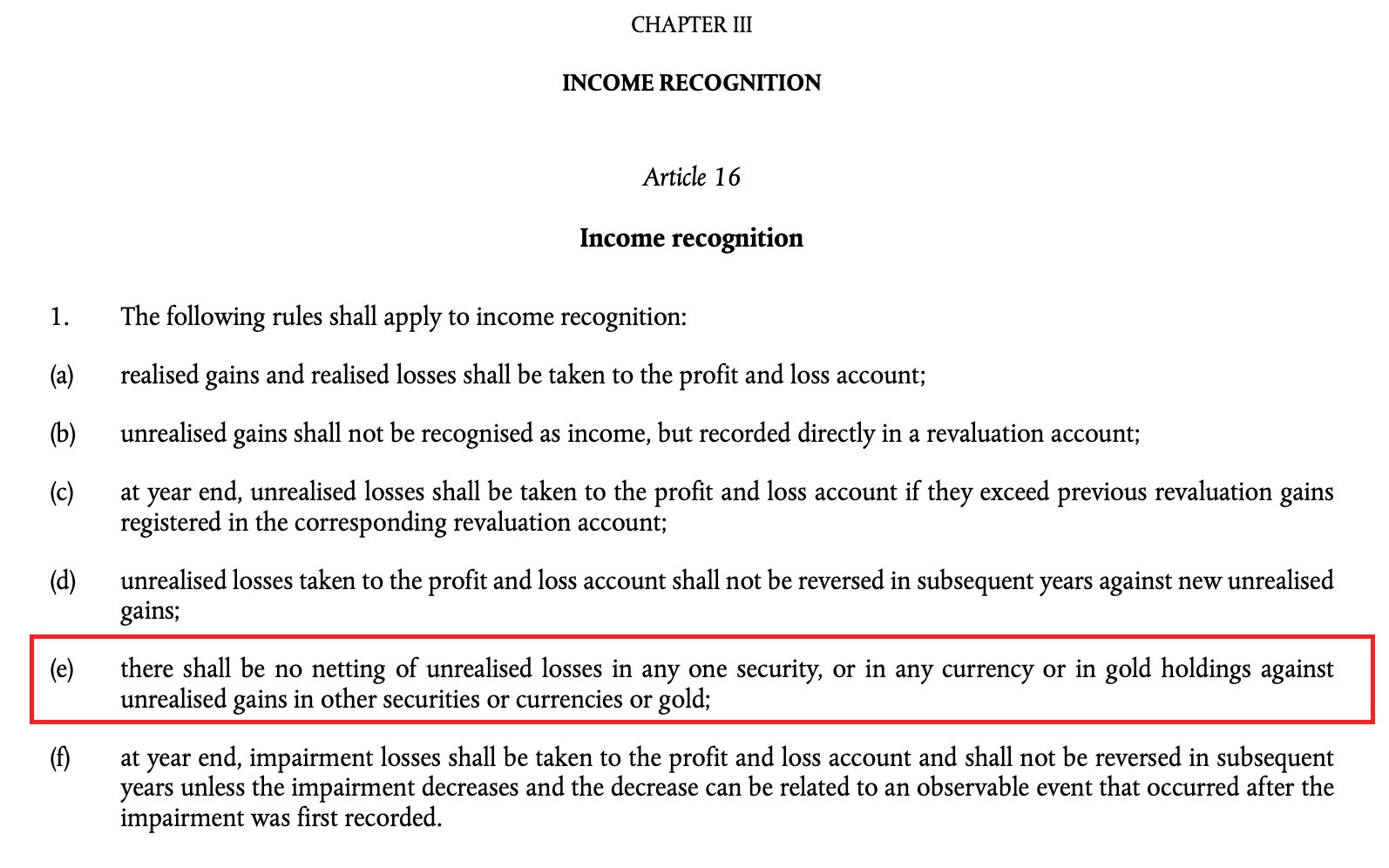

this means the ECB can only use unrealized gold gains to cover/offset future unrealized losses on gold these unrealized gains can neither offset an operational, nor a loss in another security bucket, such as FX

thus, unrealized gold gains accumulate on the ECB's liability side, under the revaluation account, and the only way they can be debited (e.g. to cover expenses, or credit an NCB's reserve account) is: 1️⃣ when the ECB sells the gold, thus turning an unrealized gain into a realized one 2️⃣ offset future losses in the gold bucket

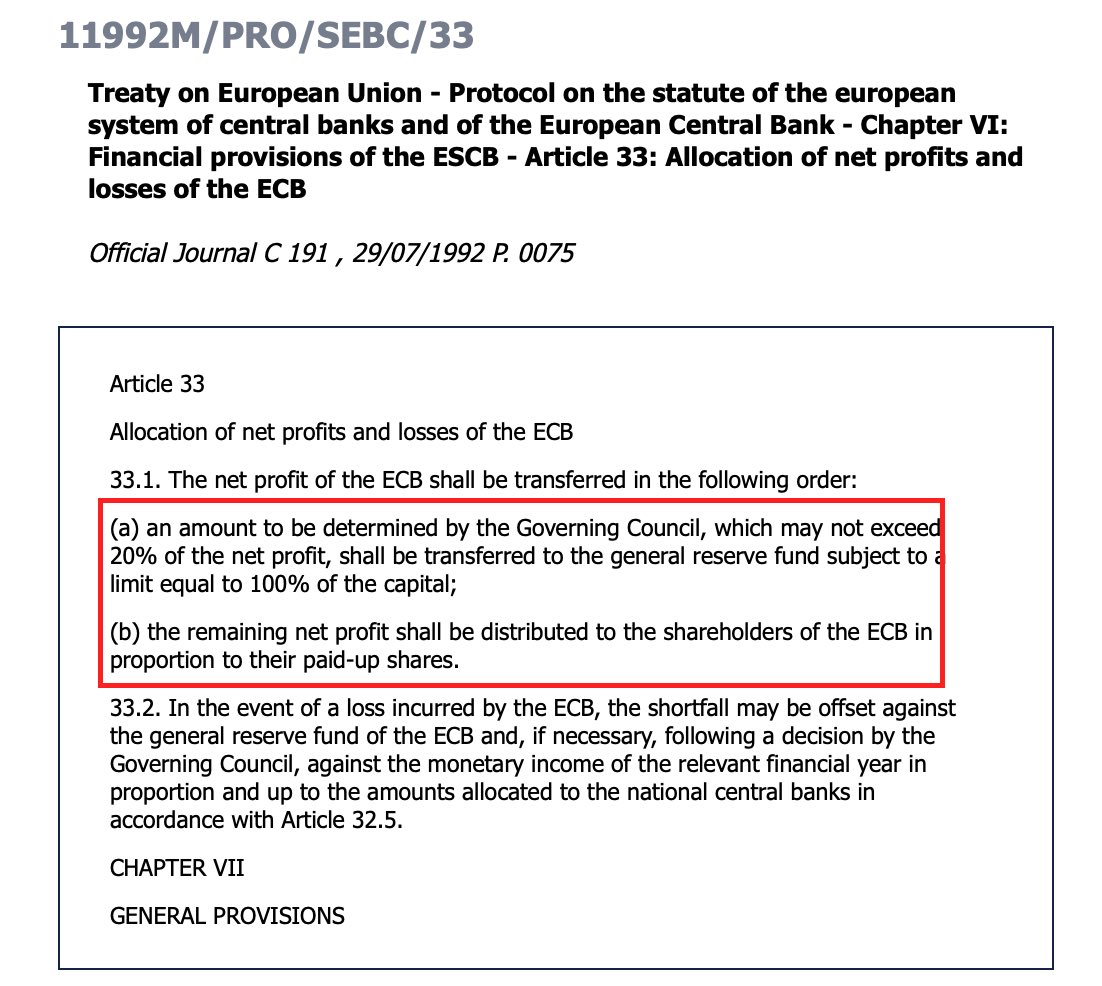

after ECB's realized gains are booked to PnL, the ECB splits up the net profit as: ➖ up to 20% to the general reserve fund, which can be used to offset future PnL losses ➖ the rest distributed to the NCB's, proportional to the National Central Bank's paid-up shares