My Thoughts

Short-form commentary on macro, market structure, commodities, Bitcoin, crypto markets, and AI.

here, the bank's assets increase by the value of the T-bill and liabilities increase by the amount that they paid you for it. in the balance sheet the T-bill will have the same value as what the bank paid you/deposited into your account

the bank doesn't need to have the money to pay you for the T-bill, as that money will be created and deposited into your account

on the bank's sheet side it works: its assets and liabilities increase in the same amount

the bank doesn't need to have the money to pay you for the T-bill, as that money will be created and deposited into your account

on the bank's sheet side it works: its assets and liabilities increase in the same amount

when a bank buys an asset from a non-bank it creates broad money

if a commercial bank buys a US Treasury bill from you, it will pay you by create a new deposit into your account

so effectively the bank pays you by creating new digital currency and crediting it into your account

when a bank buys an asset from a non-bank it creates broad money

if a commercial bank buys a US Treasury bill from you, it will pay you by create a new deposit into your account

so effectively the bank pays you by creating new digital currency and crediting it into your account

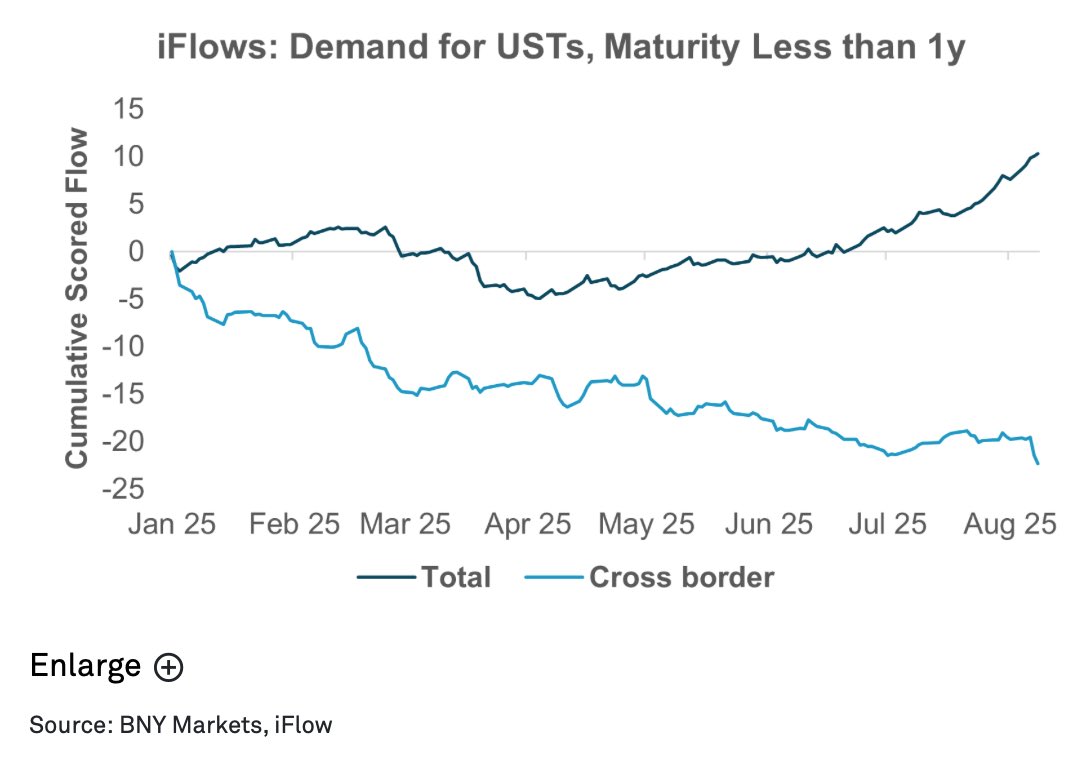

most of auctioned Treasury bills in 2025 are bought domestically

foreign investors are net sellers, so the new T-bill supply is being absorbed by US-based institutions

so most of short-term US debt is being absorbed by the US economy and not by foreign investors

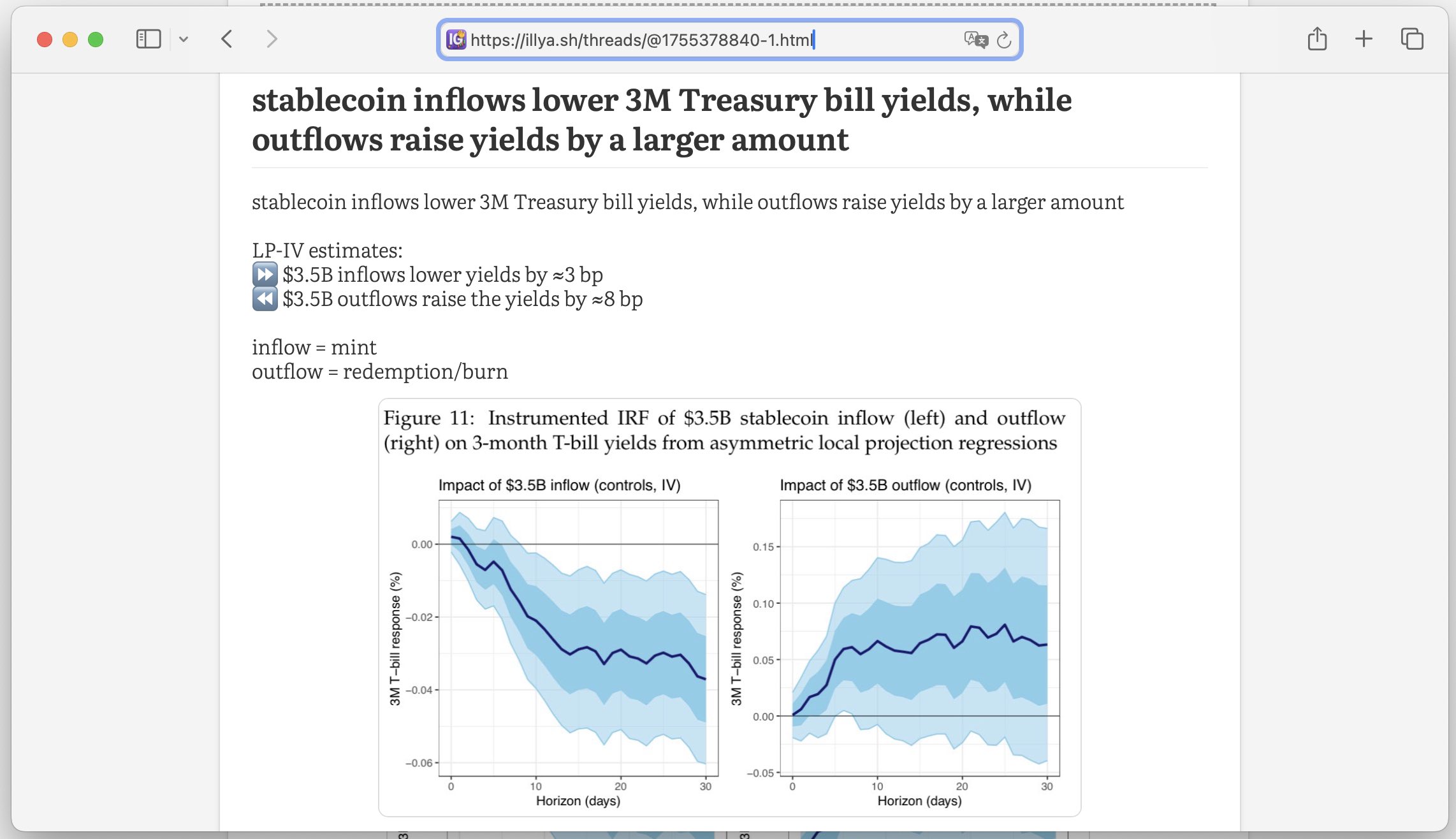

🇨🇳 China is considering Yuan-backed stablecoins, which will lower short-term CGB yields

that's assuming the stablecoin issuers will proxy short-term government bonds, like in the US

i wrote a thread explaining that. you can read it here: https://illya.sh/threads/@1755378840-1.html

the specific QE policies will vary, but it will probably include an MBS-style QE like in QE1 2008. this will lower mortgage rates short-term

I explained why in this thread: https://illya.sh/threads/@1754148538-1.html

the next burst in global liquidity/larger financial crisis will only happen after several more rounds of QE

the next round of QE is close, but hasn’t even started yet and rates were not cut. however, the next big debt refinancing is underway

the next burst in global liquidity/larger financial crisis will only happen after several more rounds of QE

the next round of QE is close, but hasn’t even started yet and rates were not cut. however, the next big debt refinancing is underway

still, at some point QE's won't be able to prevent a prolonged negative impact on the market - the top of the cycle or close to it

we're not there yet

still, at some point QE's won't be able to prevent a prolonged negative impact on the market - the top of the cycle or close to it

we're not there yet

eventually, the carry will unwind and debt needs to be refinanced

more QE-like measures will be taken, but eventually it won't be enough to prevent deleveraging/burst. this means defaults, margin calls, etc. the latter will likely be addressed by another form of QE

eventually, the carry will unwind and debt needs to be refinanced

more QE-like measures will be taken, but eventually it won't be enough to prevent deleveraging/burst. this means defaults, margin calls, etc. the latter will likely be addressed by another form of QE

in conjunction, this creates an upward pressure in the global liquidity for the near future

of course, this also builds up on leverage in the form of market-wide carry trades, and duration mismatching in the form of rolling over of debt by the Treasury

in conjunction, this creates an upward pressure in the global liquidity for the near future

of course, this also builds up on leverage in the form of market-wide carry trades, and duration mismatching in the form of rolling over of debt by the Treasury

i explained how weaker US dollar increases cross-border USD liquidity in this thread: https://illya.sh/threads/@1755216337-1.html

i explained how weaker US dollar increases cross-border USD liquidity in this thread: https://illya.sh/threads/@1755216337-1.html

weaker USD, means appreciation of FX currencies and since many cross-border bank loans are collateralized with a local currency - solvency ratios improve, thus increasing balance sheet capacity for more USD credit

this means an increase in broad money

weaker USD, means appreciation of FX currencies and since many cross-border bank loans are collateralized with a local currency - solvency ratios improve, thus increasing balance sheet capacity for more USD credit

this means an increase in broad money

i covered more this aspect of QE in my thread about how to use yield spreads to reason about future Bitcoin price and cycles

you can read it here: https://illya.sh/threads/@1755595543-1.html

i covered more this aspect of QE in my thread about how to use yield spreads to reason about future Bitcoin price and cycles

you can read it here: https://illya.sh/threads/@1755595543-1.html

once Fed does QE, reserve account balances increase, thus directly increasing base money

broad money either increases indirectly or directly if the Fed credits a non-bank institution

once Fed does QE, reserve account balances increase, thus directly increasing base money

broad money either increases indirectly or directly if the Fed credits a non-bank institution

once Fed cuts interest rates, more borrowing will occur, thus expanding broad money

it will also lower T-bill yields short-term, as the prices are bid up due to a lower risk-free rate

once Fed cuts interest rates, more borrowing will occur, thus expanding broad money

it will also lower T-bill yields short-term, as the prices are bid up due to a lower risk-free rate

a lot of these US treasury purchases will be financed with short-term rolling debt (e.g. repo)

the newly issued Treasuries themselves will be used as collateral to borrow cash, many times over via rehypothecation

a lot of these US treasury purchases will be financed with short-term rolling debt (e.g. repo)

the newly issued Treasuries themselves will be used as collateral to borrow cash, many times over via rehypothecation

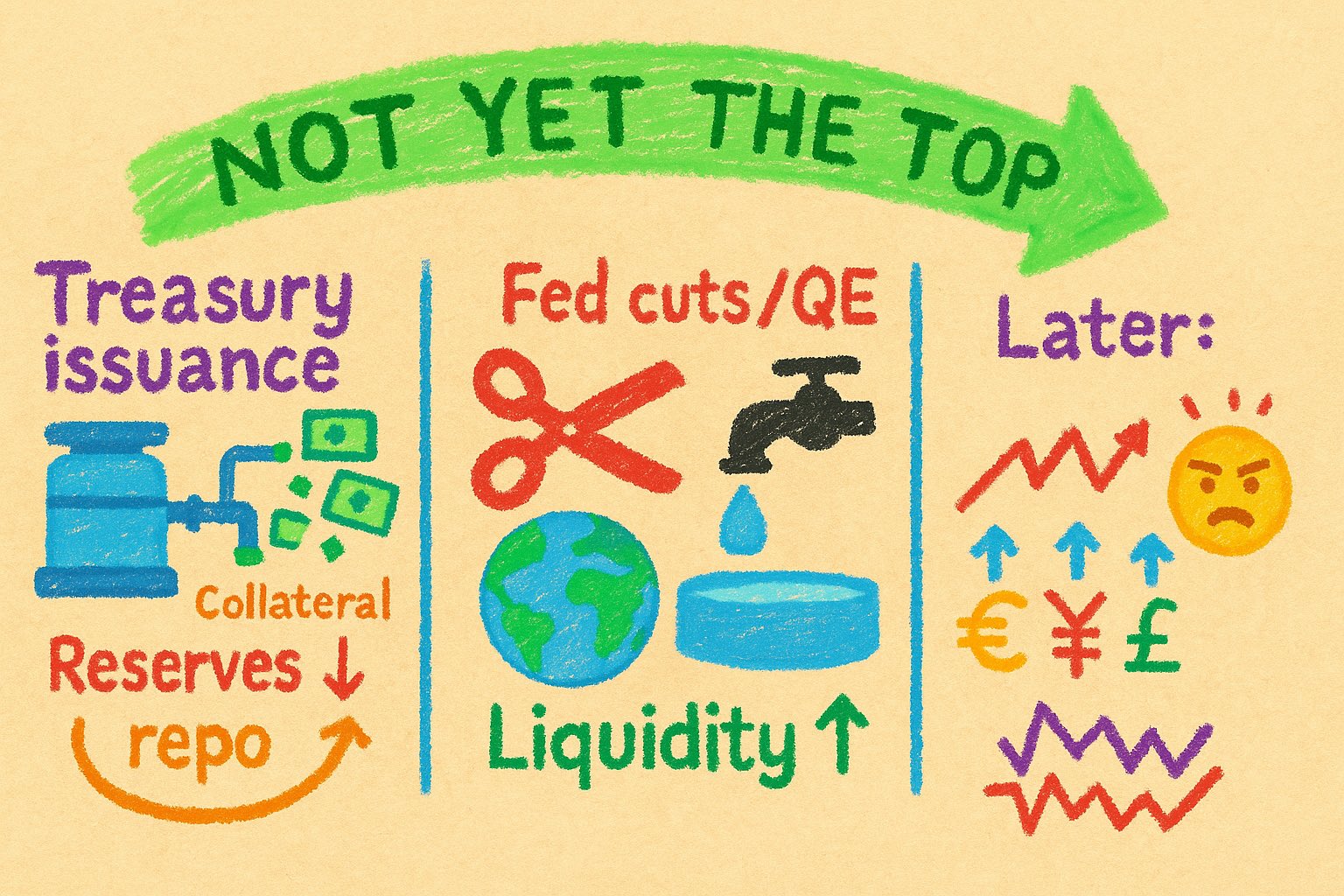

it's NOT yet the top of the cycle for equities, cryptocurrencies and other risk assets. here’s why

1️⃣ US Treasury is issuing more debt

2️⃣ in the next months I expect the Fed to cut rates and/or introduce some form of QE

3️⃣ weaker USD means more cross-border USD credit

it's NOT yet the top of the cycle for equities, cryptocurrencies and other risk assets. here’s why

1️⃣ US Treasury is issuing more debt

2️⃣ in the next months I expect the Fed to cut rates and/or introduce some form of QE

3️⃣ weaker USD means more cross-border USD credit

it's NOT the top yet - i'll post a thread with an explanation soon

stay tuned 👀

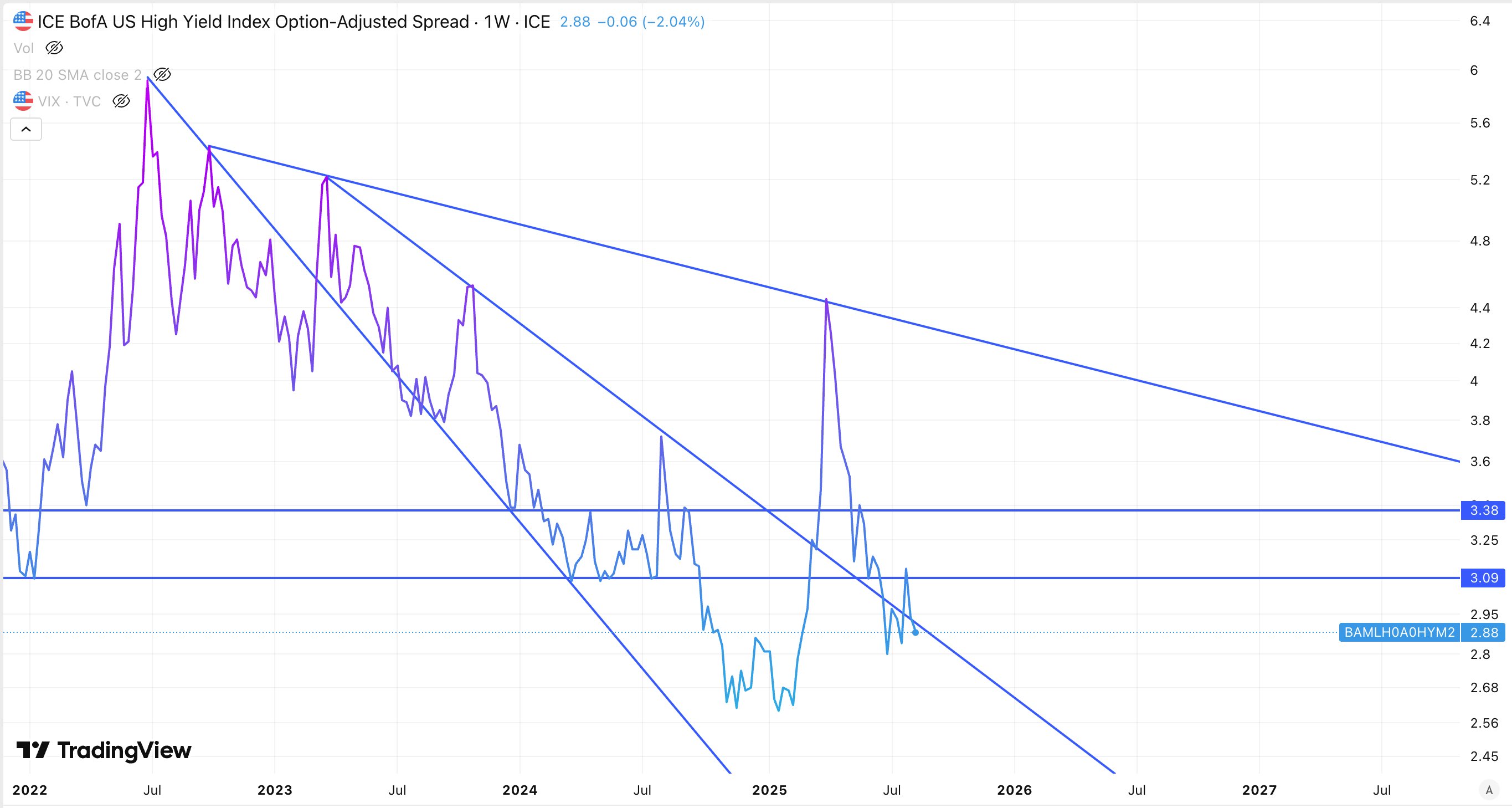

cryptocurrency prices perform well when yield spreads are low/decreasing and bad when yield spreads are high/increasing

this is specifically true when you analyze it at a higher timeframe - think monthly timescale instead of daily one. and the larger the spike/change

eventually this carry trade unwinds, and yield spreads soar. balance sheet constrains, existing positions get too expensive too roll-over/re-finance that’s where you get the big(er) financial crisis

and then you get more QE/lower rates to address that

eventually this carry trade unwinds, and yield spreads soar. balance sheet constrains, existing positions get too expensive too roll-over/re-finance that’s where you get the big(er) financial crisis

and then you get more QE/lower rates to address that

US Treasury debt is likely to be among the assets purchased by those same banks that received QE funds from the central bank. so central bank's QE injection may be used to purchase US Treasury debt at auctions, thus effectively monetizing the government debt 😁

US Treasury debt is likely to be among the assets purchased by those same banks that received QE funds from the central bank. so central bank's QE injection may be used to purchase US Treasury debt at auctions, thus effectively monetizing the government debt 😁

even if it doesn't happen directly at the start - eventually QE also increases broad money, due to reduced balance sheet constraints and an increase in cash reserves, which needs to be invested ASAP. this leads to more lending and asset purchases

even if it doesn't happen directly at the start - eventually QE also increases broad money, due to reduced balance sheet constraints and an increase in cash reserves, which needs to be invested ASAP. this leads to more lending and asset purchases

initially QE may only increase base money supply - as commercial banks reserve balances get credited by the Central Bank

if the Central Bank purchases assets from non-bank financial institutions, then broad money increases directly as well, as deposits increase

initially QE may only increase base money supply - as commercial banks reserve balances get credited by the Central Bank

if the Central Bank purchases assets from non-bank financial institutions, then broad money increases directly as well, as deposits increase

the US Treasury may also issue more debt to increase the supply of safe assets, thus offsetting the compression shock

end result: more safe assets/prime collateral provided to markets. remember that the newly issued treasuries are likely to be rehypothecated several times

the US Treasury may also issue more debt to increase the supply of safe assets, thus offsetting the compression shock

end result: more safe assets/prime collateral provided to markets. remember that the newly issued treasuries are likely to be rehypothecated several times

the global financial system depends on the abundance of this collateral, otherwise - defaults, margin calls, etc

i wrote a thread/article explaining how US Treasuries are the dominant collateral in short-term wholesale debt markets (e.g. repo). read here: https://illya.sh/threads/@1751726431-1.html

the global financial system depends on the abundance of this collateral, otherwise - defaults, margin calls, etc

i wrote a thread/article explaining how US Treasuries are the dominant collateral in short-term wholesale debt markets (e.g. repo). read here: https://illya.sh/threads/@1751726431-1.html

QE also removes safe collateral from the market, mainly US Treasury bills, notes and bonds. this safe collateral is the backbone of wholesale debt markets, where financial institutions, including commercial and central banks finance and re-finance their positions