Global liquidity: the hidden force behind asset prices

Asset prices follow liquidity. These articles explore how money flows through the system — from central bank operations to money market funds, cross-border USD credit, and the mechanics that connect it all to what you see on your screen.

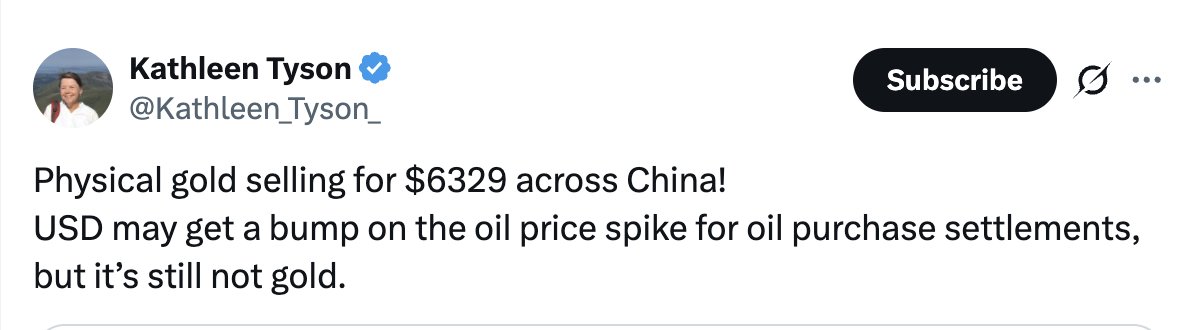

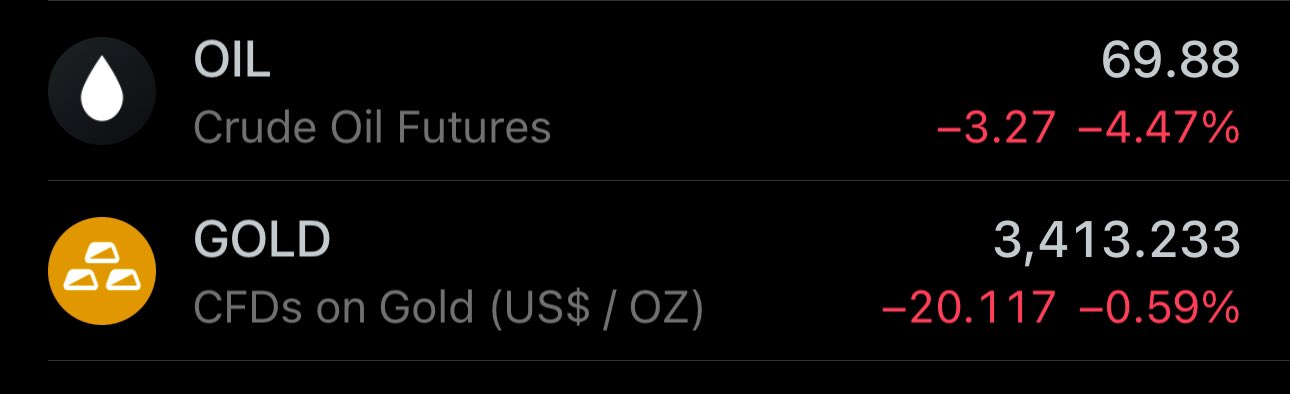

Why High Oil Prices Are Bad For USD (HINT: China & Credit)

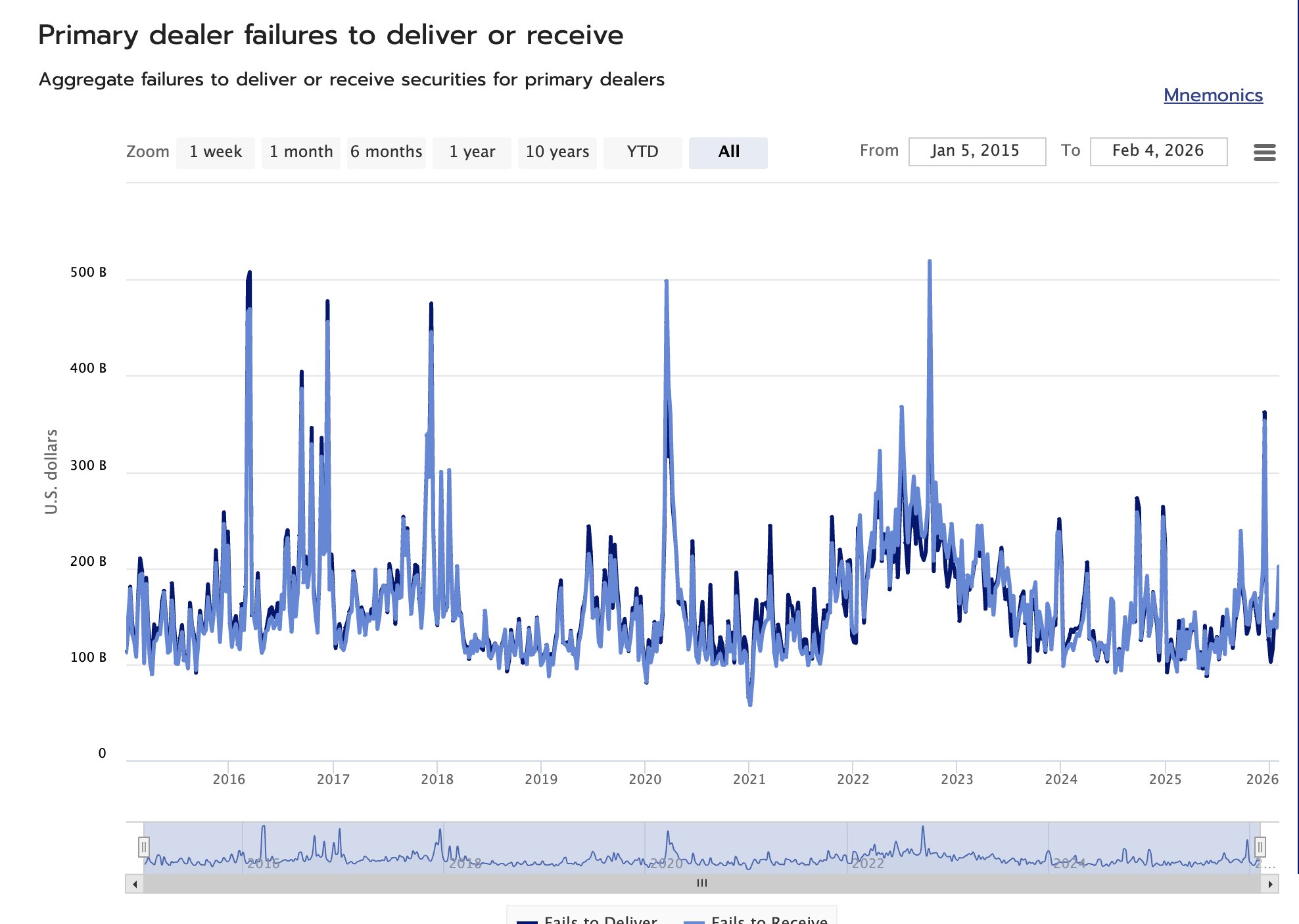

Primary Dealers Failures To Settle Implications For Risk Assets

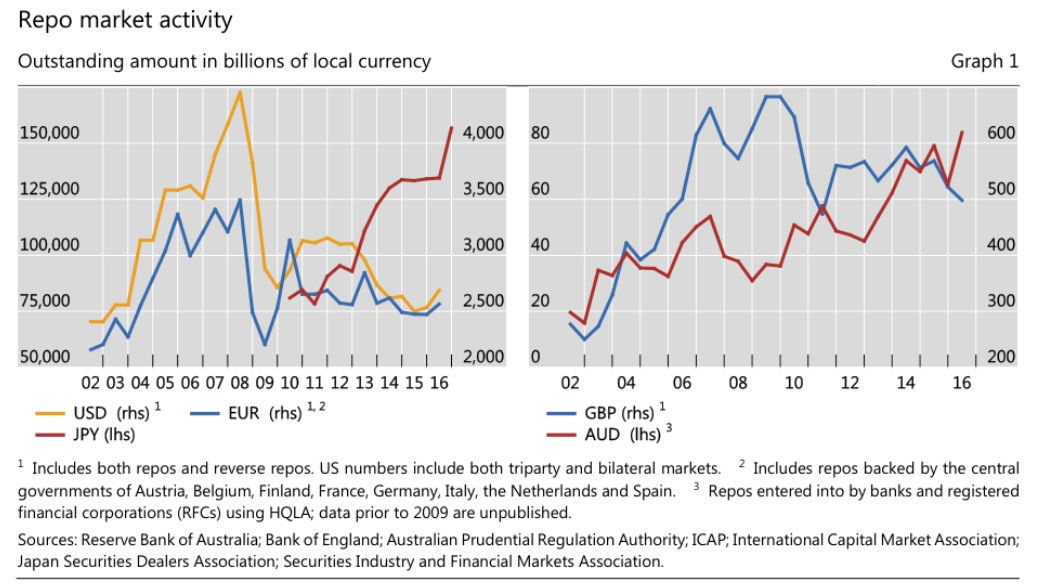

M2 Money Supply Is A Bad Measure of Global Liquidity

'The market is never wrong' #8

How Banks Create Money When Purchasing Assets

my article on repo rates and BTC price was referenced on bitcoin.com

lower interest rates means less attractive repo and deposit rates, thus expect more capital movement into assets, as the yields on MMF/deposits become less attractive

gold is a great asset to hold for the next 5 years

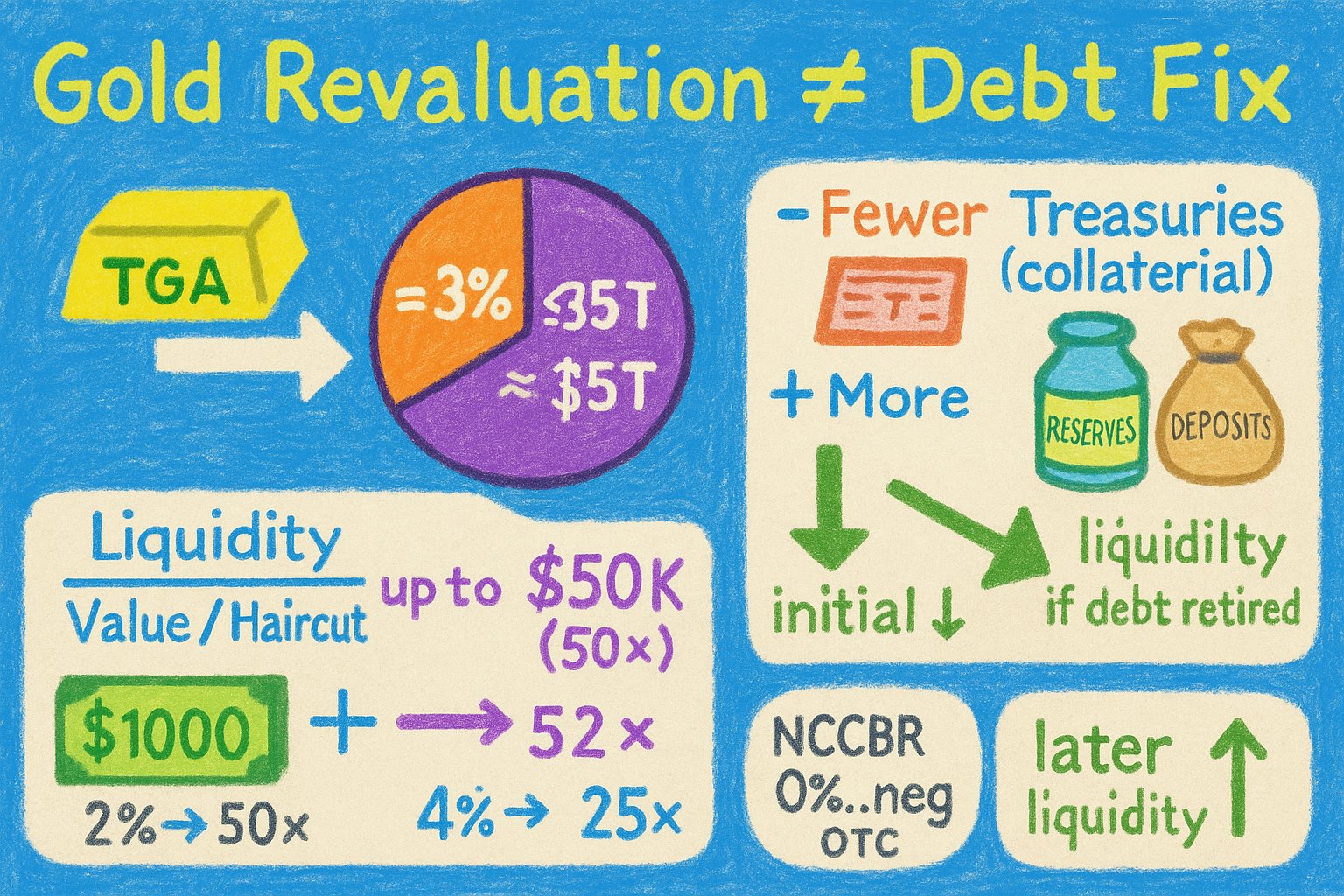

gold revaluation will NOT solve the US debt problem

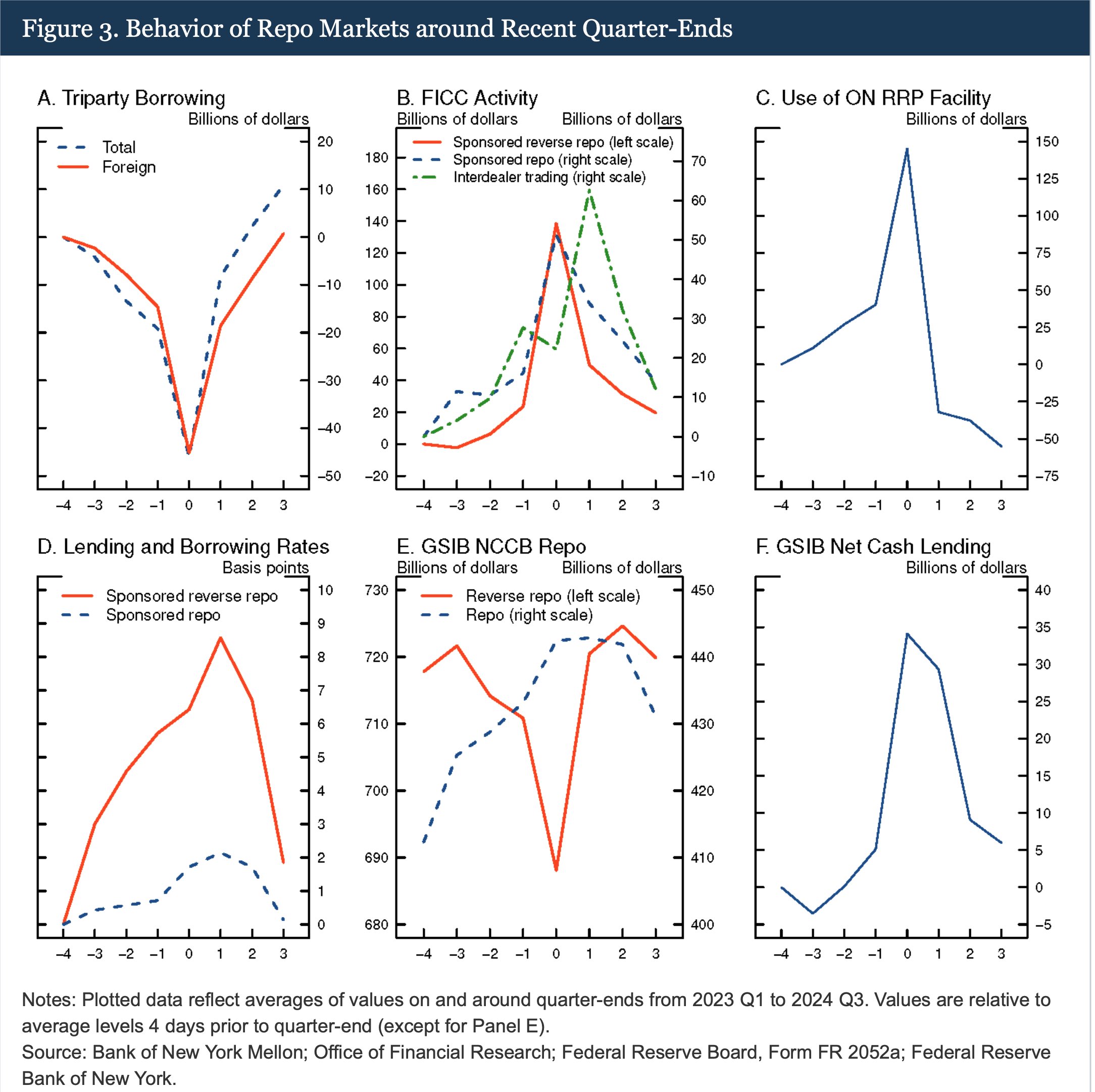

repo rates increase and borrowing decreases in quarter-ends

when a bank buys an asset from a non-bank it creates broad money

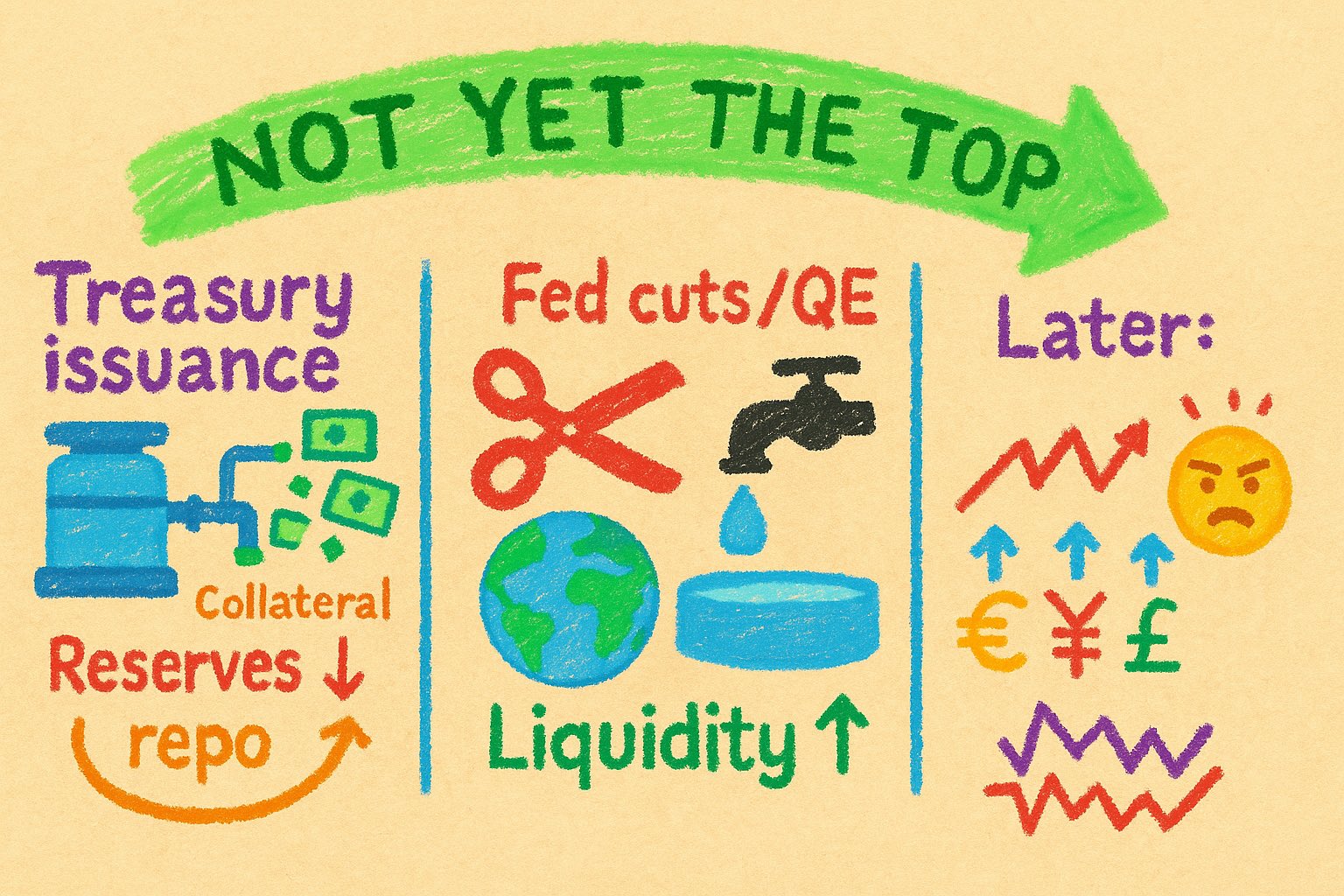

it's NOT yet the top of the cycle for equities, cryptocurrencies and other risk assets. here’s why

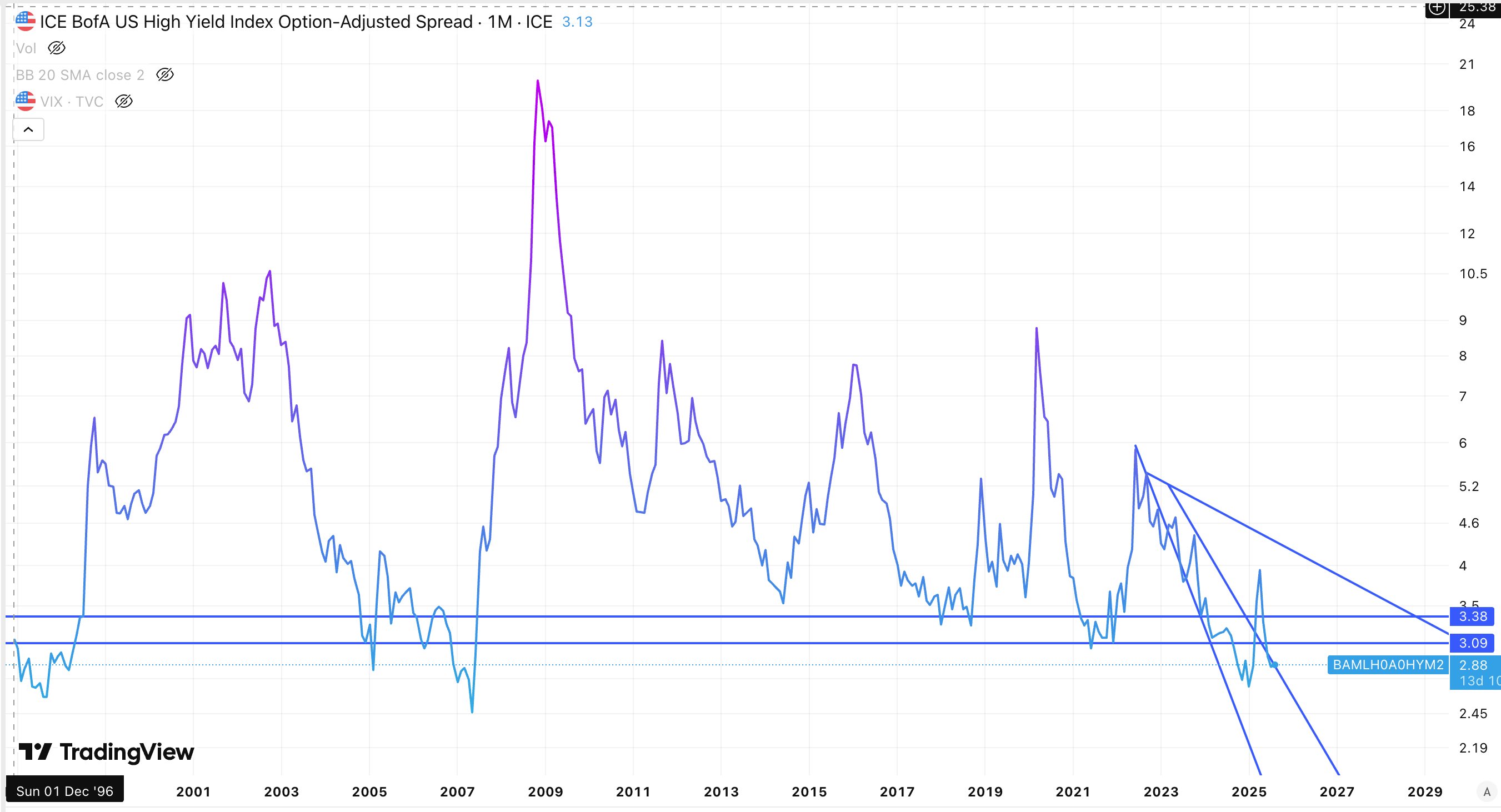

here's what yield spreads are saying about Bitcoin

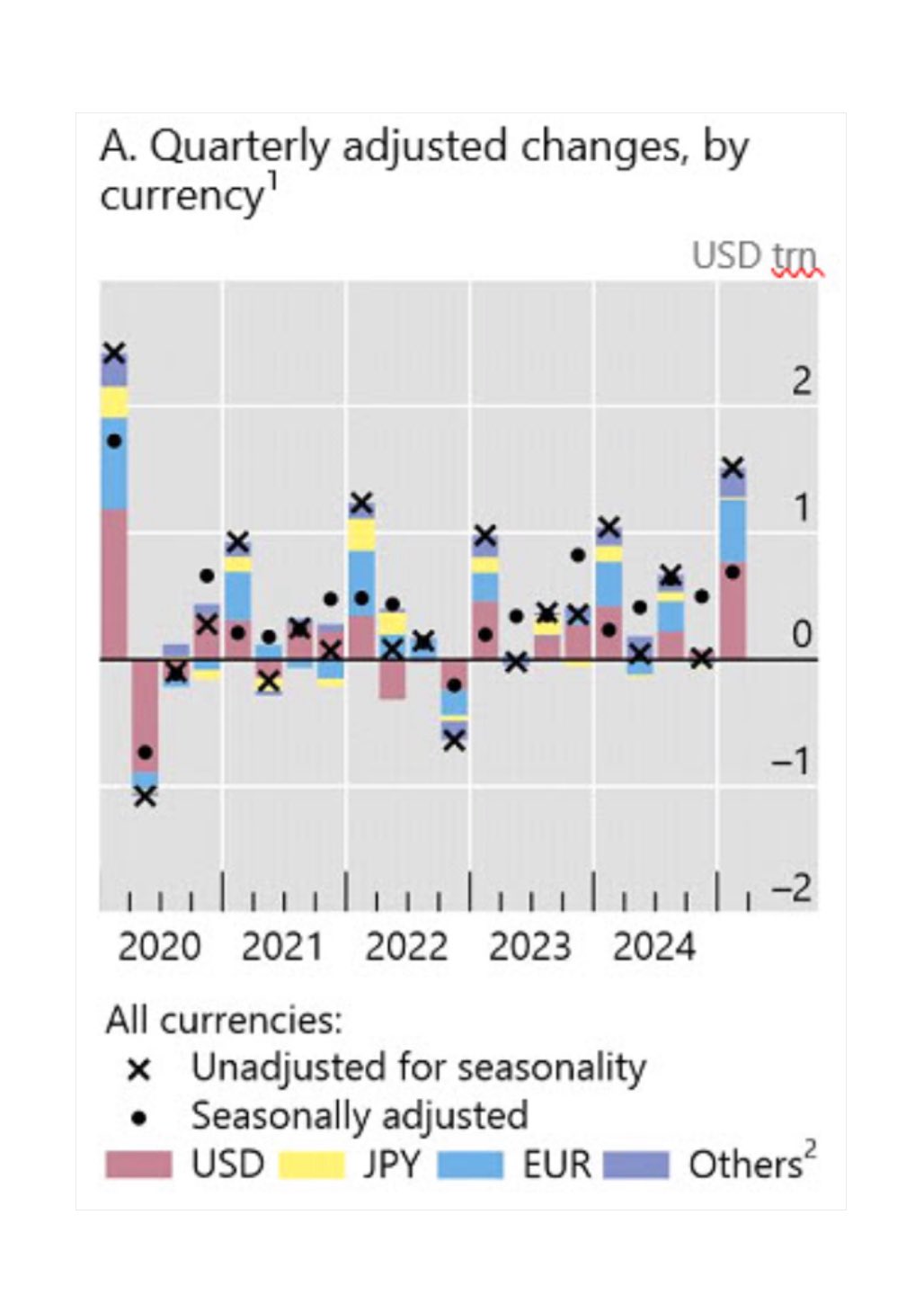

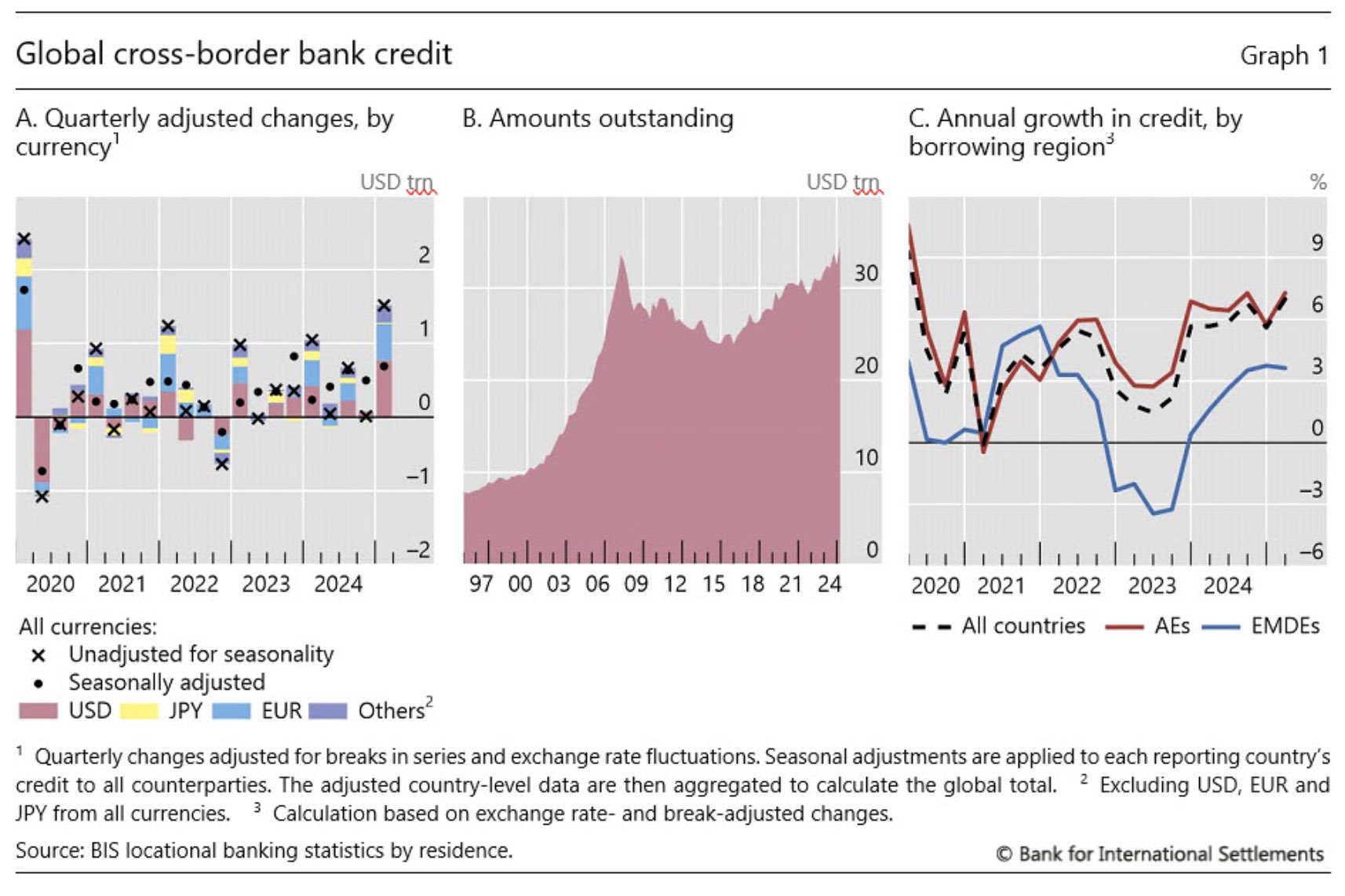

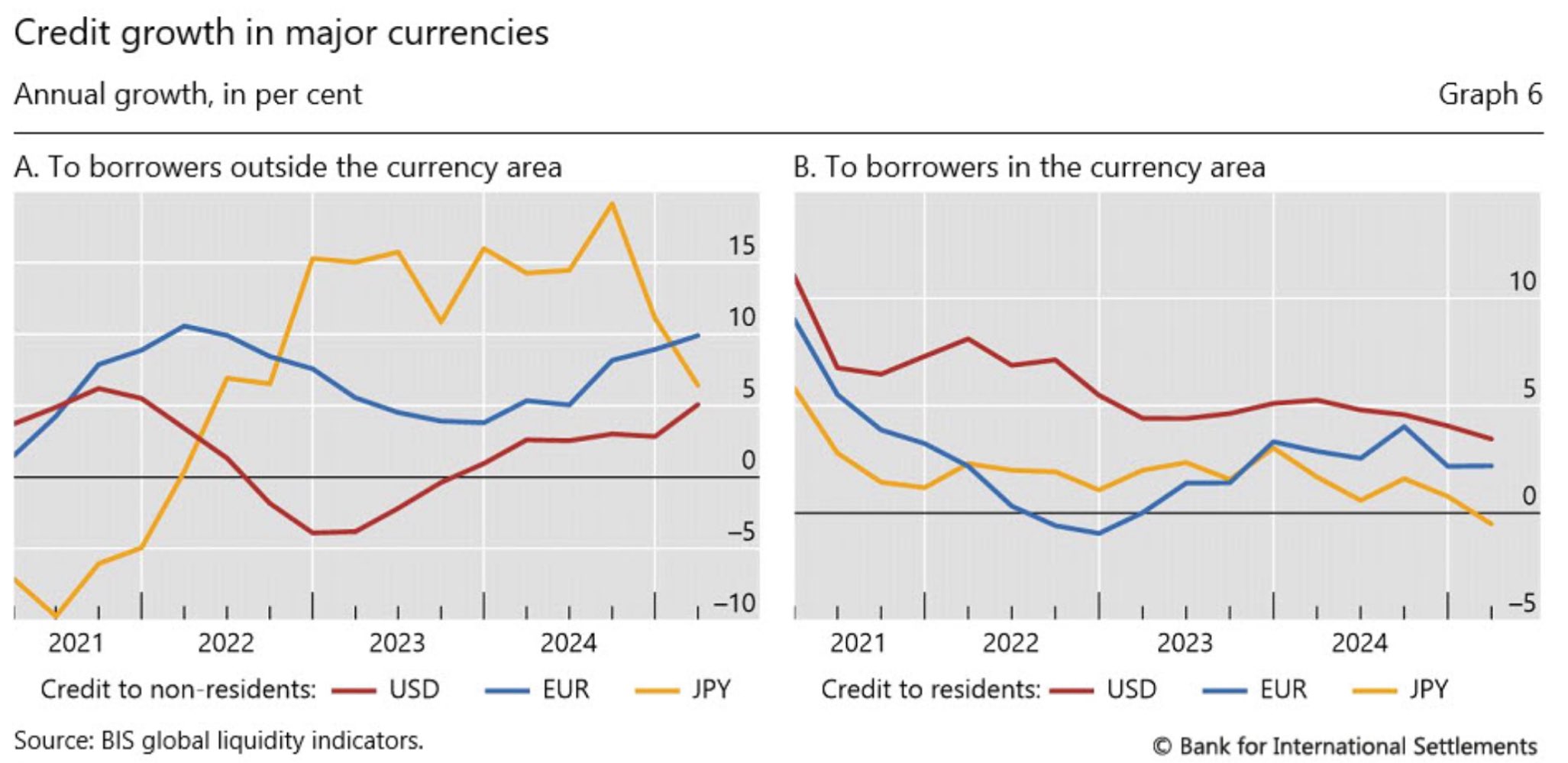

USD cross-border bank credit grew by $800 billion in Q1 2025

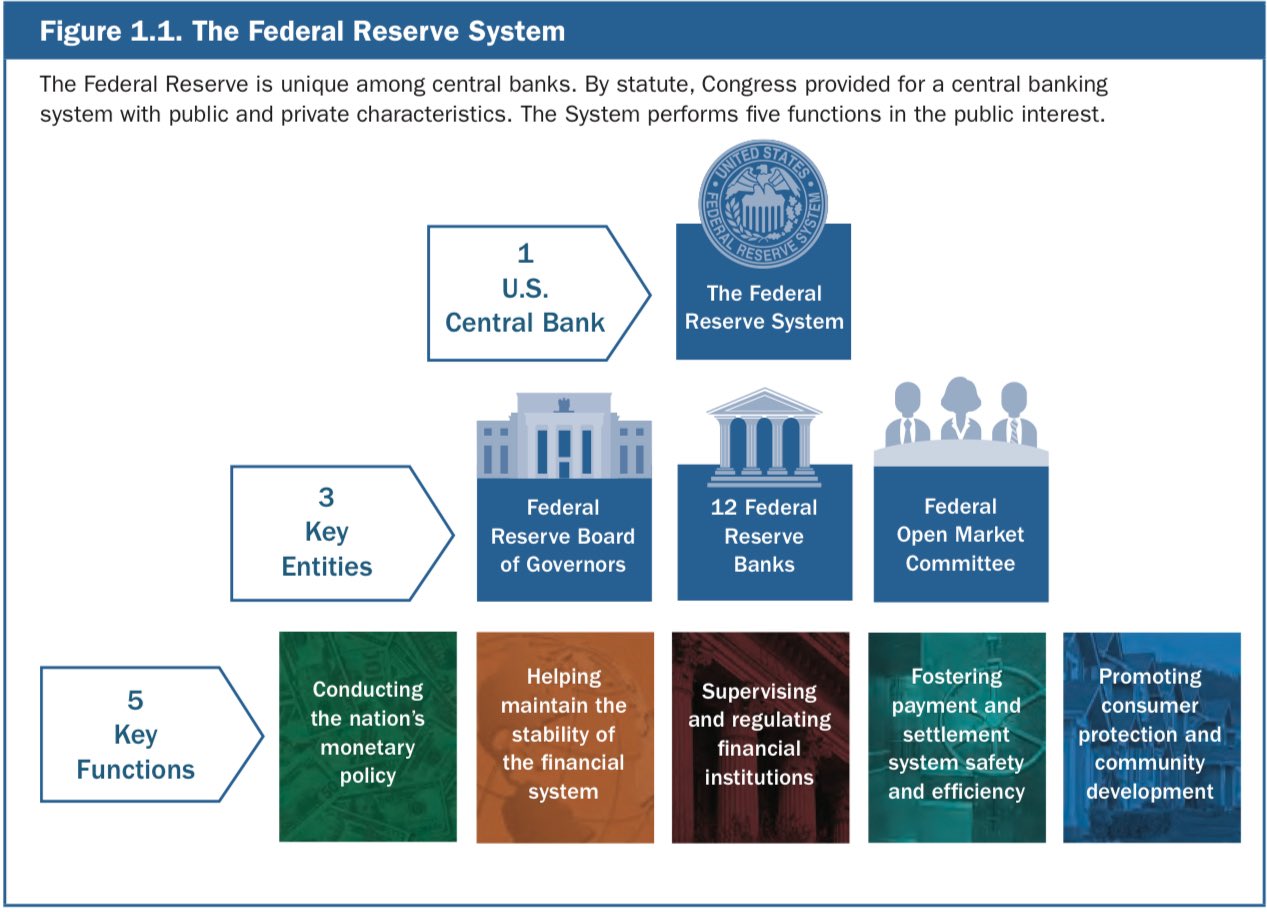

by "central bank" I'm frequently referring to the broader set of the legal framework behind the macro monetary policy

outstanding cross-border bank credit reached a record of $34.7 trillion

weaker US dollar means more USD credit issuance abroad - here's why

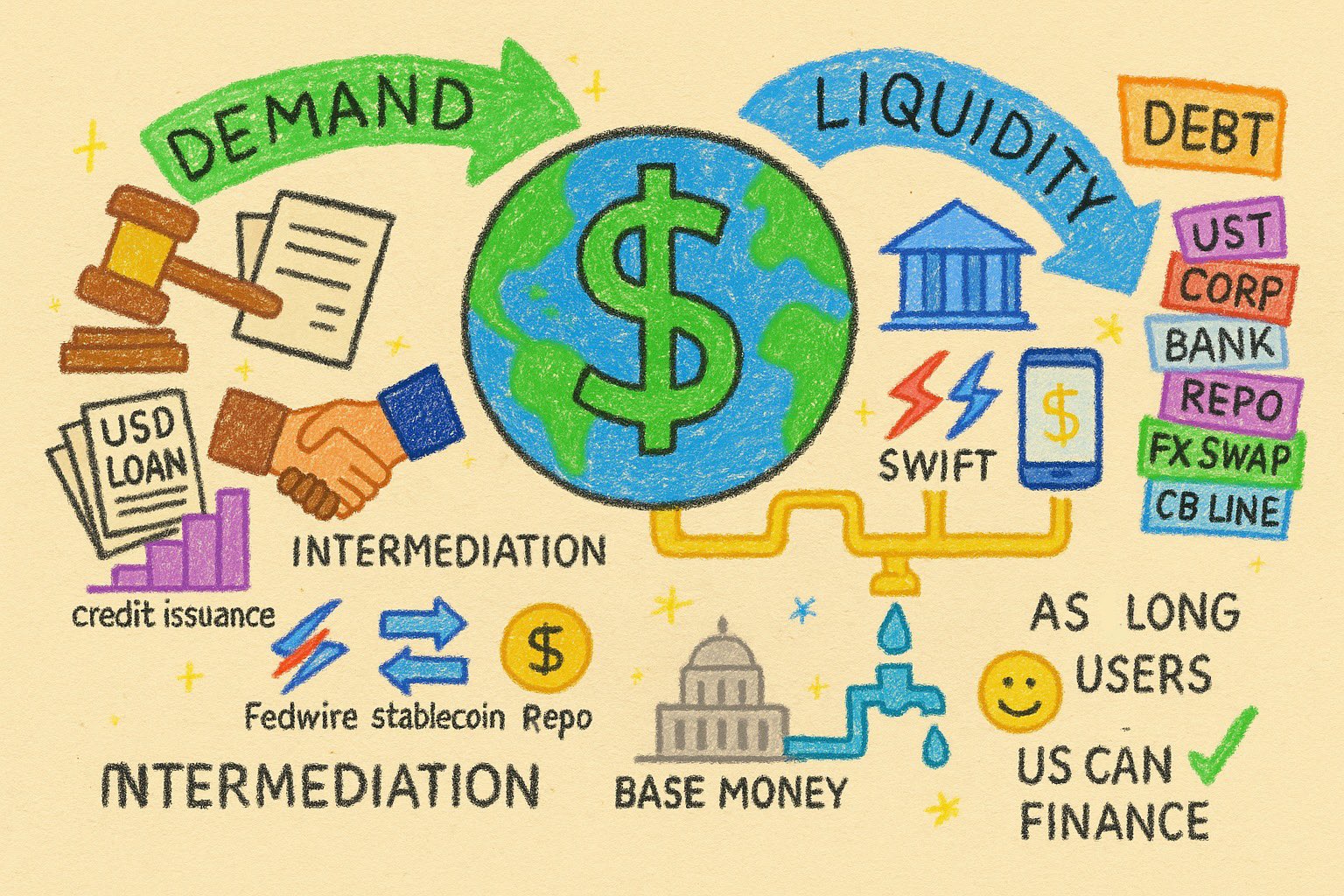

USD is the world's reserve currency, but what does that mean?

now imagine when credit institutions can tokenize new credit and allow automated stablecoin issuance backed by that credit

'The market is never wrong' #7

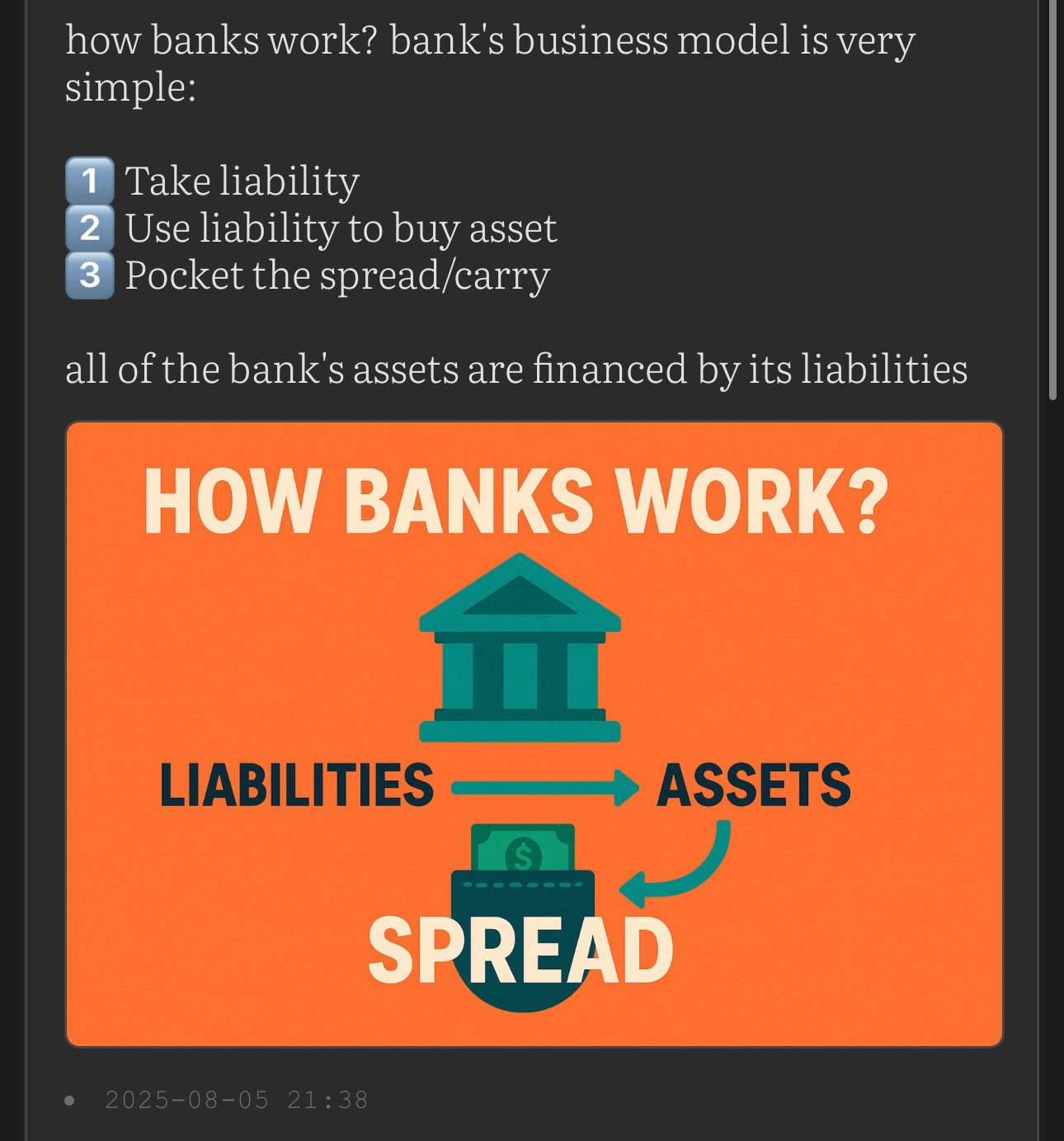

how banks work? bank's business model is very simple:

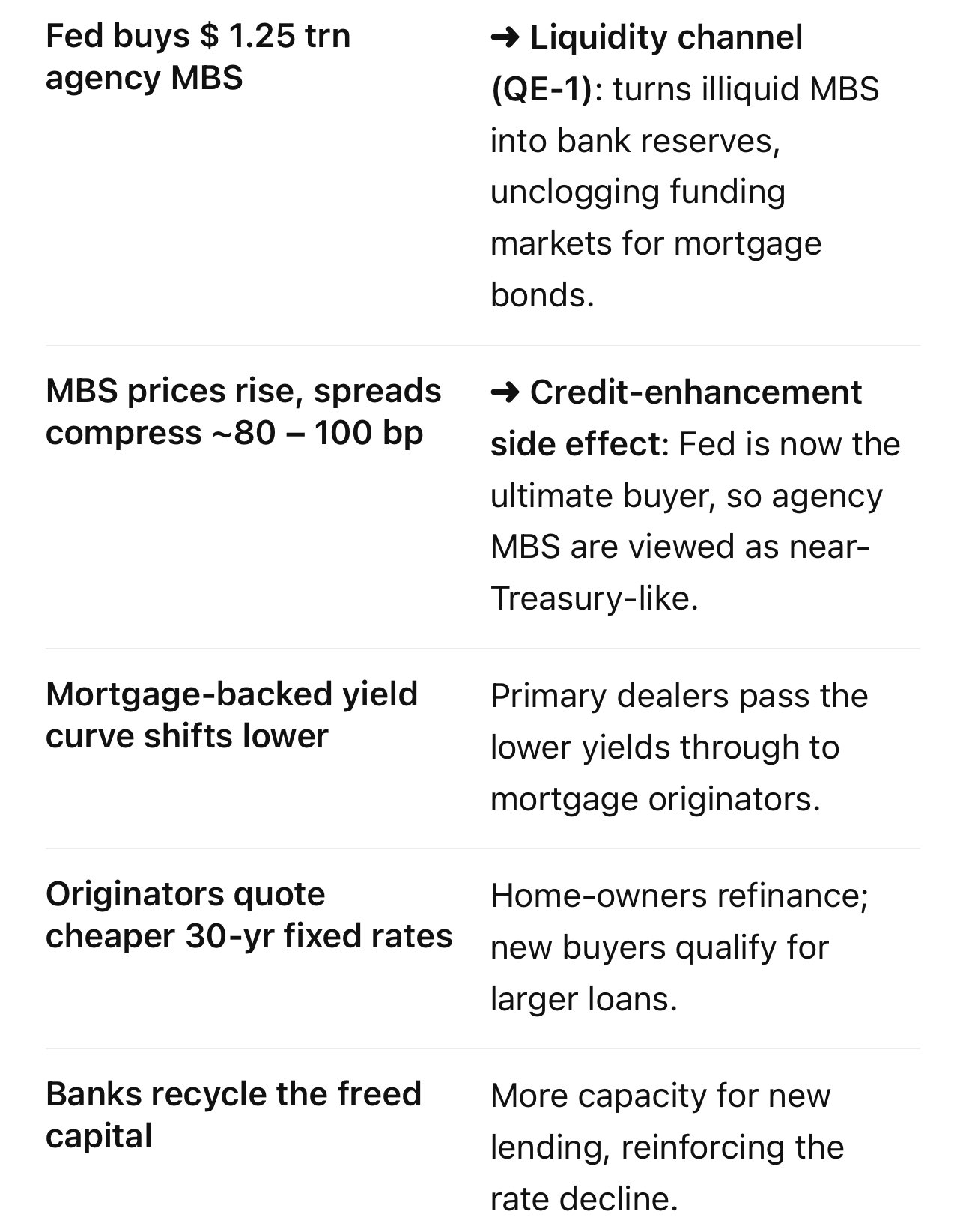

to lower the mortgage rates the Fed can purchase agency MBS - likely they did in QE 1 2008

regulations may sound boring - but they're crucial to understand money, liquidity and financial system as a whole

'The market is never wrong' #6

🇨🇳 china's central bank uses USD value as a key driver in economic policies #2