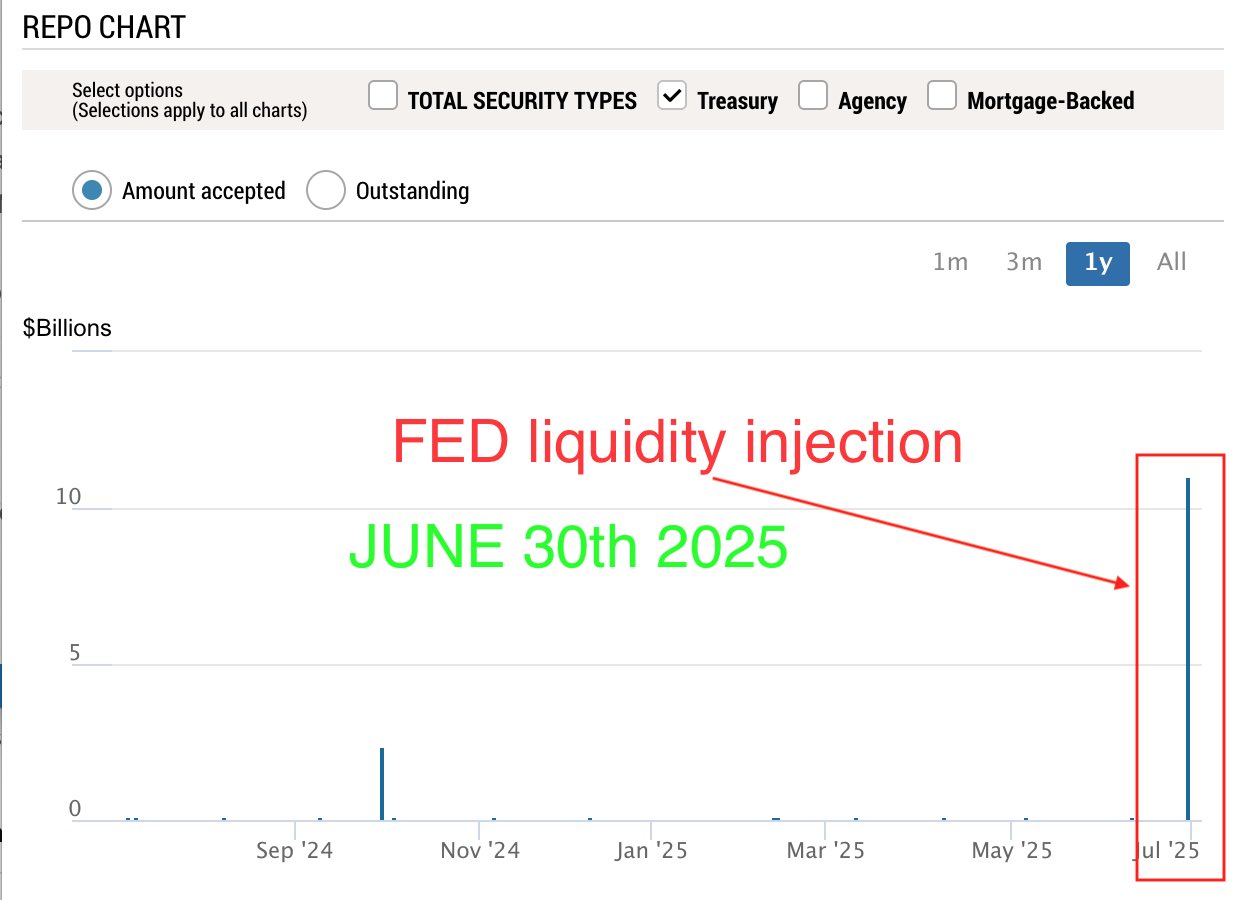

🚨FED just injected $11B of liquidity #1

🚨FED just injected $11B of liquidity 👉 TL;DR: interest rate cuts & QE incoming $11B is insignificant - but it's an early sign: there is a lack of liquidity/cash if undressed, will lead to systemic defaults. existing debt needs to be refinanced the fix/what's next? see TL;DR

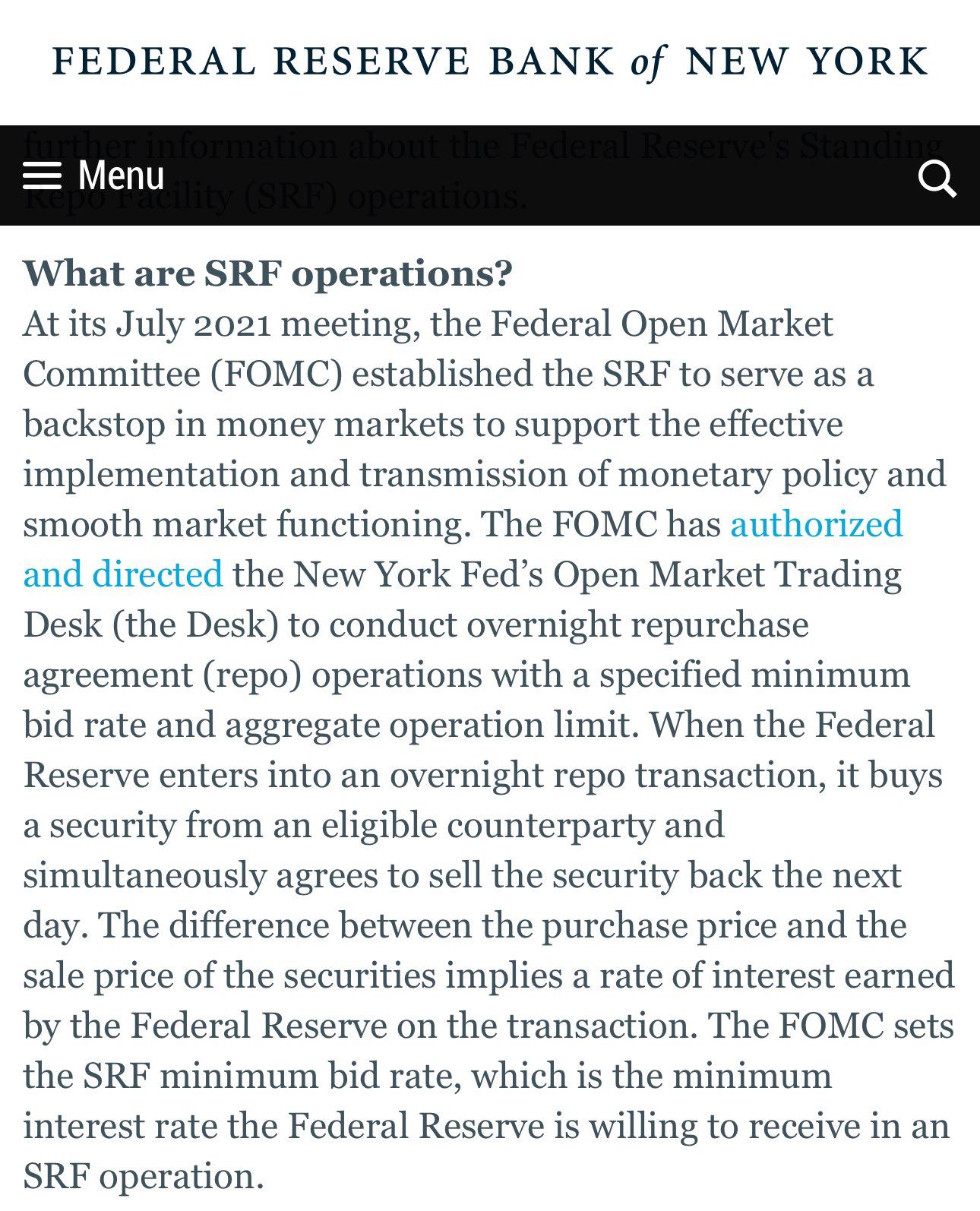

SRF provides daily $500B liquidity limit for overnight repo operations a rate is published daily & dealers lend borrow against US bonds dealers/market makers use SRF when the rate in the open repo market gets too high SRF = Standing Repo Facility

with SRF the FED sets an upper limit on repo market rates most of the collateral is US Treasury bonds this exerts downward pressure on bond yields - by preventing sell-offs

in practice, FED's SRF is used when there is a scarcity of liquidity/cash the market has US bonds & needs cash, so lenders increase rates SRF sets a daily rate. if that rate is smaller than in the smaller repo market - the dealers instead borrow USD directly from the FED

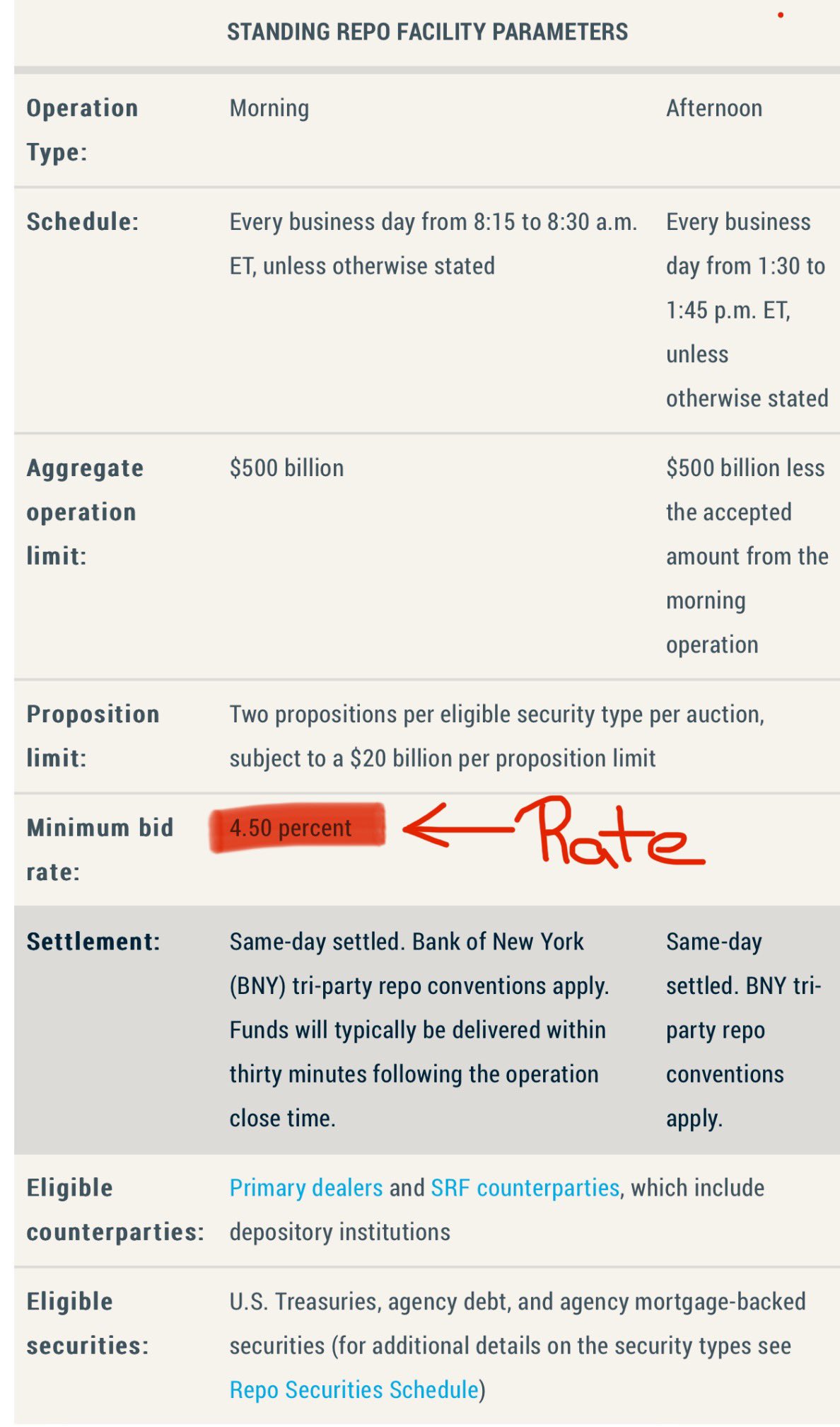

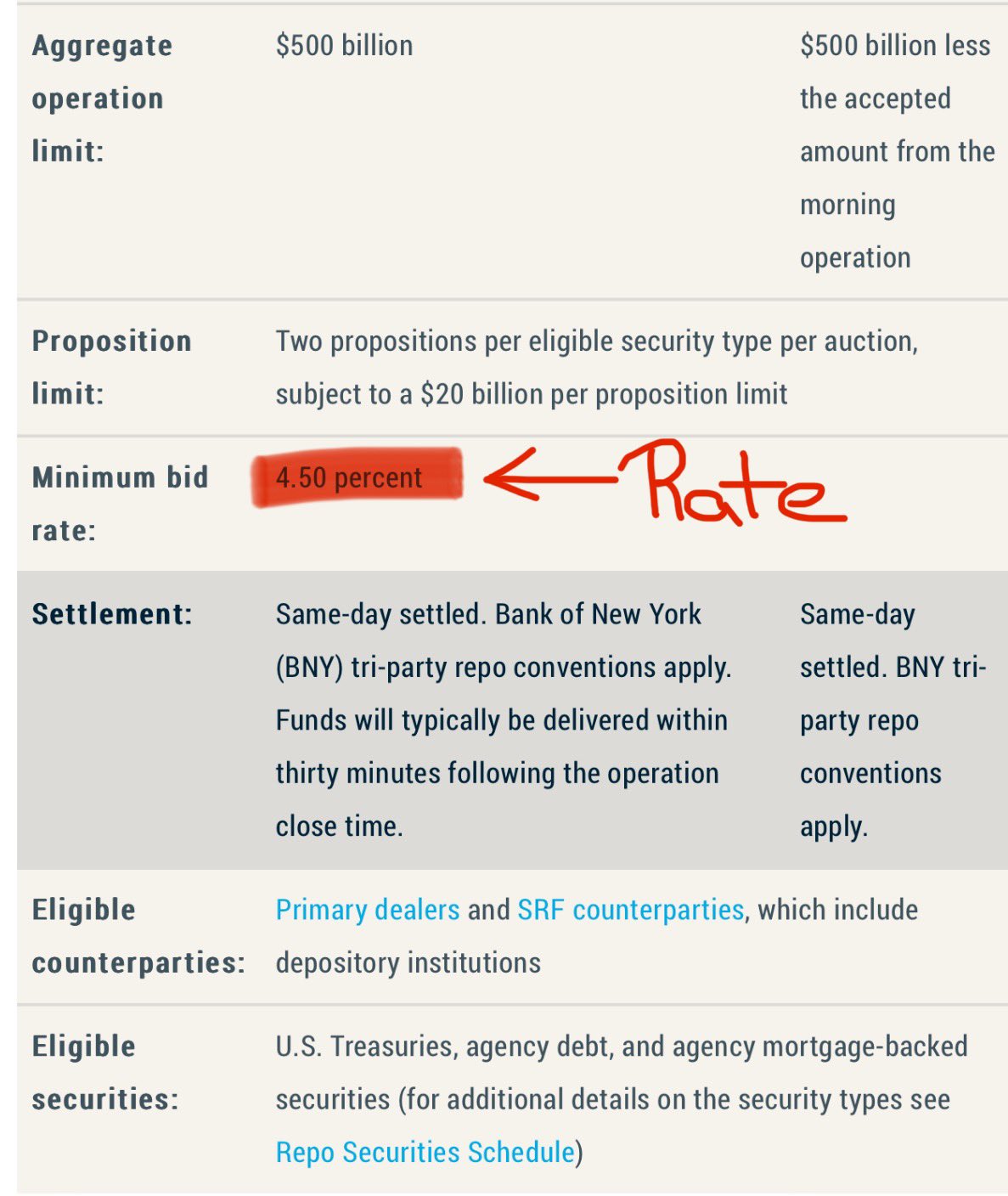

current SRF minimum bid rate is 4.5% that's the annualized rate that the federal reserve sets requires dor overnight repo loans via Standing Repo Facility dealers/market makers can borrow cash against US treasuries for 1 day at ≈4.5% annualized directly from the FED

not only US treasuries are accepted as collateral for SRF dealers/market makers can use: 1️⃣ US. Treasuries 2️⃣ agency debt 3️⃣ agency mortgage-backed securities agency debt instruments aren't issued by US Treasury, but by government sponsored enterprises (GSE) & federal agencies